Have you ever looked at your bank balance towards the end of the month and asked where did all my money go? I know I have…too many times. You can’t remember anything substantial that you bought, and other than paying bills, you’re not sure where your hard-earned money went. Come to think of it, am I even keeping track of my bills? Do I know exactly how much I spent on groceries this month? Where do I even begin tracking expenses?

When you think that most of us spend 8-10 hours, 5 days a week earning this money, it seems crazy to think that we don’t take more care of it. But still, most of us don’t. It’s not spoken about – it’s not polite to ask other people how they keep track of their money and God forbid if we asked for help, admitting that we aren’t actually great at it.

Tracking expenses gets a bad rep. I get it – on the one end of the scale, it’s boring, but on the other, it can induce feelings of shame, embarrassment, anxiety and frustration. But the unfortunate truth is this: keeping track of your money allows you to create a meaningful and realistic budget, face and change your spending habits and save and invest more money.

It’s going to be more difficult to not do it. Think about becoming healthy without tracking your weight or the inches off your waist – it’s not impossible, but it’s more difficult to figure out how far you’ve come without going through this process. And you know what’s worse? Looking at a meagre amount (or a negative amount) in your bank account and wondering where your money went.

On the contrary, tracking where your money goes is the foundation of all other wealth-building strategies and will make budgeting and saving flow easier – it is the 20% in the 80-20 equation (the theory that 20% of the work yields 80% of the results). The good thing is that you can create systems that suit you and the process of tracking expenses can be simple, straightforward, and effective.

2. How do I track my finances?

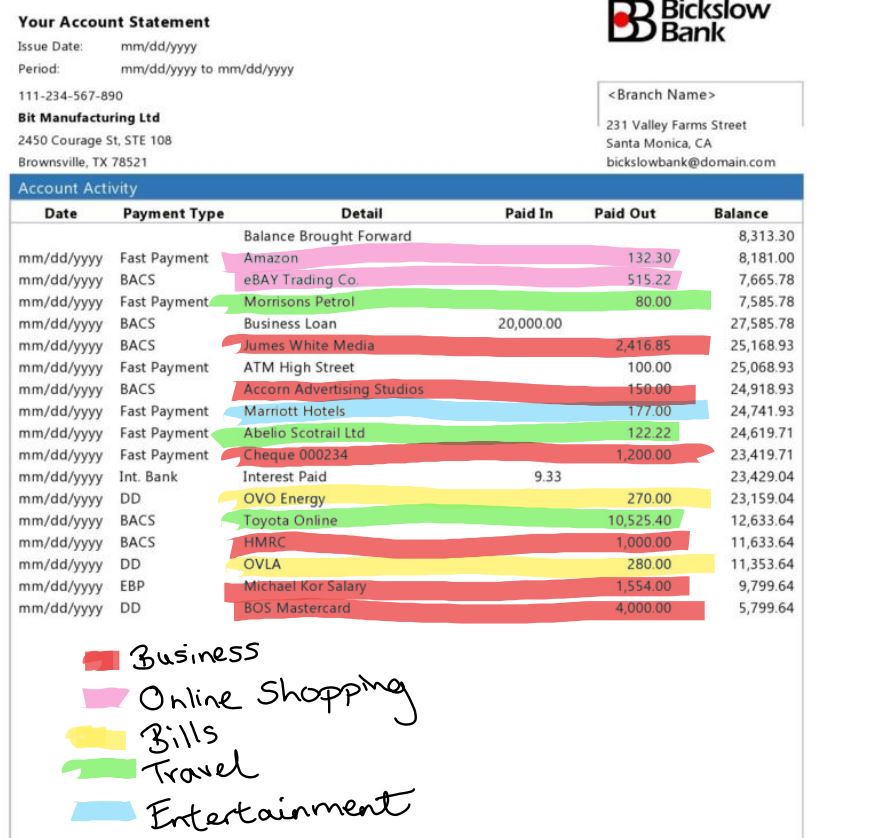

There are three main methods to track your spending in the long term. Whichever method you use, the first step is the same. To get started you are going to need your last 1-3 months of bank statements and receipts, preferably printed out, and a highlighter and pens. As you scan through your expenses, highlight ones that naturally ‘fall’ into the same category in a certain colour, for example groceries.

Some spending won’t naturally fall into a category; for example, renewing your annual subscription to your internet security software or purchasing printer ink. I would start off with more categories and gradually narrow it down; for example, your printer ink might align best with stationery or office equipment. Your categories will be highly personal – some people like very specific categories to closely monitor their spending, whereas others prefer general sweeping categories to keep a bird’s eye view.

3. What expenses should I track and budget for?

Generally speaking, expenses might fall under the following category titles:

Rent or mortgage

Utility bills

Phone/internet

Insurance

Tax

Groceries

Household items/ products/ décor

Dining out

Entertainment

Medical

Gifts

Fuel/transport

Children (clothing, activities, toys etc.)

Clothing/ toiletries/ grooming

Subscriptions

Pets

Travel/holidays

Charity

Of course, you may have more or fewer categories than this, depending on your spending patterns and habits. Once you have worked out your categories (which can and will change over time so don’t worry if they aren’t perfect), you need to calculate the totals for each category – this budget tracker has a built-in, readymade expenses calculator. This will help you to create a realistic budget that you can actually stick to. When you have reached this stage, choose one of the methods below to track your money.

4. What is the best way to track my spending?

4a. Tracking monthly expenses using excel

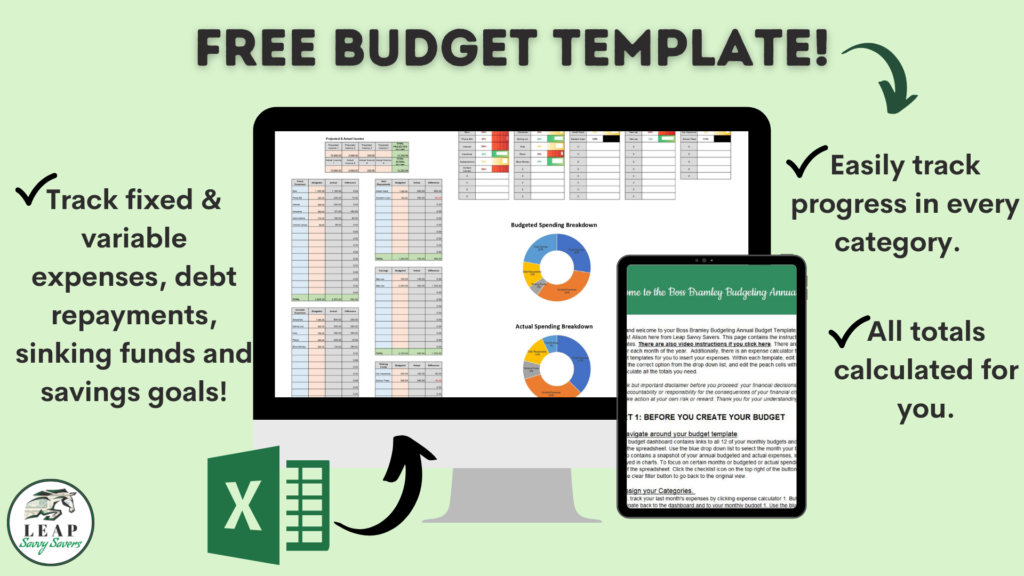

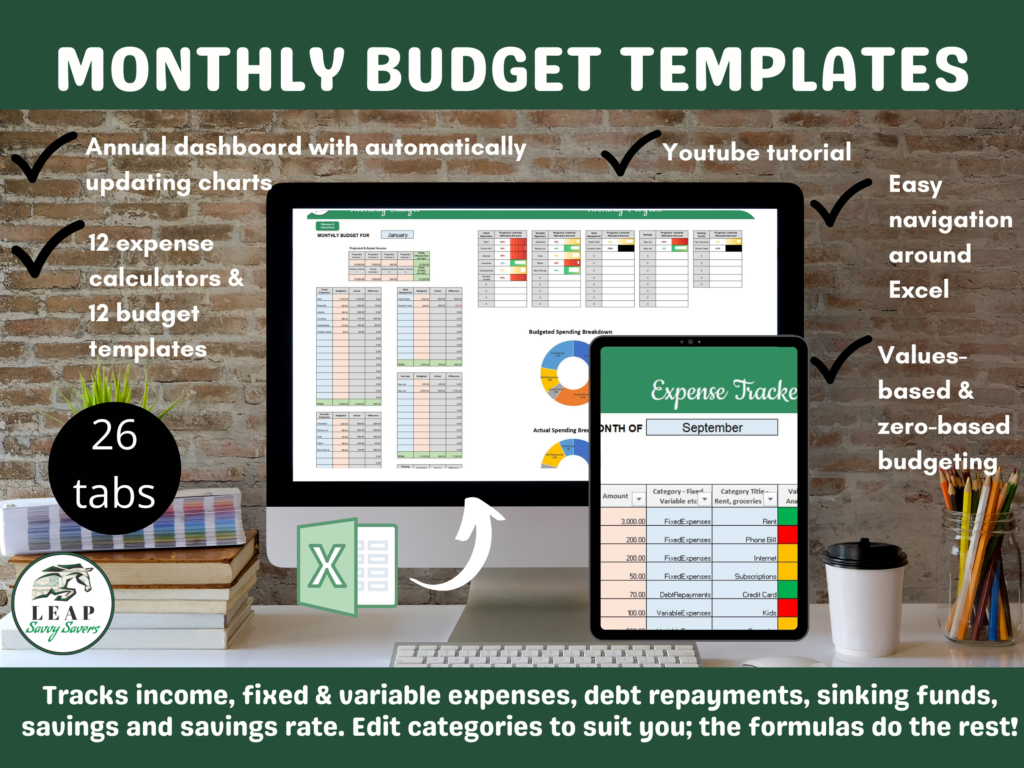

Using Excel is my preferred method, so I will explain why this strategy is Excel-lent first! I love Excel (or Google sheets) because once you have your spreadsheet set up, the formulas do all the calculations, so you just have to plug in the numbers to the expense tracker template. In this quick demo video, I show exactly how you track expenses on my monthly budget spreadsheet.

Essentially, you assign sub-categories to each of the following umbrella category headings: fixed expenses (don’t generally change month-to-month), variable expenses (varying expenses like eating at restaurants or buying clothing), debt repayments, savings (your cash savings goals such as new car or holiday) and sinking funds (if you don’t know these yet, don’t worry, leave them blank for now, but in a nutshell, they are large expenses that you can spread out and budget for over a year).

When you create a line item in your monthly budget spreadsheet (e.g., rent), it will automatically populate in a drop-down menu on the expenses calculator sheet. Simply type in your expenses on the expenses calculator sheet from your bank statement or receipts and assign them to a category.

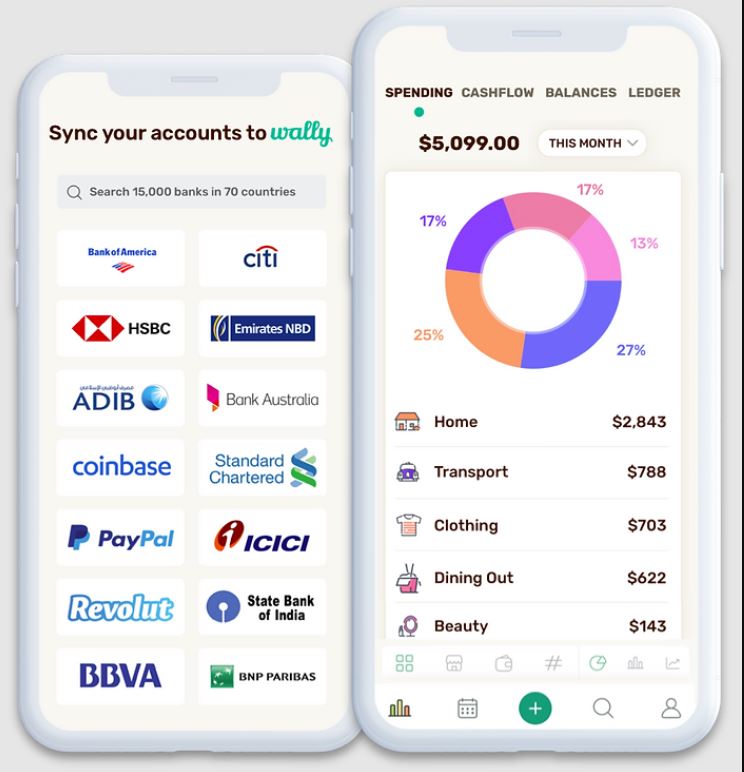

Another easy and effective way to track your spending and your bills is by using an app. There are various apps available – paid apps like YNAB allow you to link bank accounts, eliminating the step in which you input your expenses into Excel.

Others are free, such as Fudget and Wally, and readily available in the UAE. Wally has been growing rapidly since 2021 when it began allowing its users to link UAE bank accounts and is possibly the best app to track your expenses if you’re living in the UAE. Once you link your bank accounts, you can create budget categories and track your expenses within the app.

However, despite how convenient using an app may be, and how lock tight their security is, I personally still have reservations about linking all my bank accounts to an app and giving the app that much personal information.

That’s why I created my own system using Excel, which mimics all the app features, except one: with my system, you have to track your expenses manually, or at least, type them in to the spreadsheet. But I think this is a good thing. The act of doing this allows me to take a second to interact with that spending and while I am tracking my expense, weigh up how much value I assign to that interaction – how much joy or regret does it bring me to track that money?

4c. Tracking money using pen and paper

Some people prefer using pen and paper to keep a record of their money, and if that’s you, why not? It may take a little more time, but if it suits you, then you should stick to it. To use a budget notebook, I would simply write out the date, the expense, the category and the amount, and ensure that I total it. This template is a useful place to start tracking your expenses.

5. How often should I track my expenses?

This is a another highly personal question. When I started, I would track daily. It helped me gain clarity and control at first, when I felt that my spending was out of control and impulsive. I now track my expenses on a monthly basis at a minimum, so as to reconcile with my budget allocations and create a new budget for the next month. I also track my expenses if I’m having a bad day or feeling overwhelmed as managing my money helps bring a sense of control and peace to my life – I can practise conscious gratitude for the money flowing to and from me.

However, you decide to track your expenses, one thing is clear: the system must be easy for you to follow and sustain over the long term. This is not a quick fix; this is a lifestyle change and the road to building wealth for you and your family for multiple generations.