One of the most frequently asked questions of expats is ‘what’s the best way to transfer money internationally?’ Expats earning in different currencies than their home currency may have to send money home to support family or meet financial obligations in their home country. In addition, people earning in currencies such as the UAE Dirham (AED) and wanting to fund investments in brokerages that don’t accept AED often want to know the best way to exchange money.

The first thing to consider is what constitutes ‘best’ for you. For some, it’s the lowest cost money transfer, for others convenience is top of their list and for different people safety and reliability of the exchange house. Or it may be a combination of these factors. Quite often, as with most things in life, the cheapest methods are not the most efficient or reliable.

how do i find the best exchange rate?

There are some general costs to consider no matter which method of currency exchange you choose. Keep them in mind as you do your research and ensure before you decide on your exchange method, you have factored in all of the potential costs end to end.

1. International Transfer Fees

You may be charged a fixed fee for exchange, or a percentage of the amount transferred. Either way, some sort of charge is likely to be levied for the exchange by the bank or financial institution doing the currency conversion.

2. Exchange Rate

This one often tricks people. If you see an extremely low (or even free) fee for exchange, check out the exchange rate. Exchange rates vary depending on the supply and demand in the market. Some currencies are ‘pegged’ or fixed, for example the UAE Dirham is pegged to the USA dollar, meaning that they move together.

A ‘spot rate’ or ‘mid-market rate’ is the current asset value, or truest exchange rate possible. However, most banks or financial institutions add a spread to this true rate to increase the charges to you. That way, they can decrease their ‘fees’ but still make money from the exchange; it just won’t be as obvious.

For example, every $1 USD is worth 3.67AED. If every $1 cost you 3.8AED, you could buy less dollars with your dirhams. To simplify this for the purposes of this example:

If you were to buy $10,000 at 3.67AED, you would part with 36,700AED. If you were to exchange at 3.8AED, you would pay 38,000AED. This fractional increase in the spread has just cost you 1300AED. So, when people talk about getting the best possible exchange rate, this is what they mean. The closer it is to the ‘mid-market rate’, the better deal you are getting.

3. Intermediary bank fees

When doing an international transfer, an intermediary bank is often needed. To transfer money, banks must have an account with each other. If the bank you are transferring to doesn’t have an established relationship with your bank, an intermediary will be used and will charge a fee. This is usually around $15-30.

4. Recipient bank Charges

If you transfer to another person via a wire transfer, the bank will often ask you who will bear the fees – the sender or the recipient. This is because the destination bank charges a fee to receive the funds. it’s *usually* cheaper to accept all charges from the sender and you will be able to see how much the total cost will be before you go ahead with the transfer.

Most Efficient way to Transfer Money internationally

It’s best to work out all these potential costs on each method of transfer, then weigh up the best option for you. For example, some financial institutions may give you a better exchange rate but charge a higher fee. You can then decide which is the best overall for your circumstances.

Many expats begin investing into some sort of retirement funds when they move to the Middle East. Often the brokerages do not support their earned currency. You may feel confused or overwhelmed by the thought of investing due to the process of transferring and exchanging money. We often hear ‘keep fees below 1%’ but if you are subject to bank wire transfer fees, you may be paying 4% or more just on transfer, and that’s before you have factored in any sort of charges or commission for actually purchasing your stocks or bonds. So, should we just save in cash while we live overseas and not bother investing? Absolutely not!

There are ways to keep your costs down – some more efficient than others. Here are some common methods that expats use to exchange money. A disclaimer and word of warning though: the fees and terms and conditions of each of these methods is continuously changing and being updated. Therefore, I recommend you do your own research as while I aim to keep my blog up to date, I don’t update every change as soon as they happen. If you get to reading this and the terms and conditions or fees have changed, let me know and I will update the information. Otherwise, take this as a general guide or starting point for your own research.

Secondly, I have not personally used all of the methods discussed below. Some of the information is from my own experience, but much of it is from my research, talking to clients and reaching out to the companies listed. Therefore, if you have a contradictory experience of fees or service etc., please do share below to help the community have a well-rounded and up to date knowledge base to draw from.

1. Bank transfer

This is likely to be the most efficient and reliable as well as most expensive method of transfer. Most banks support international transfers through their internet banking systems – you just have to fill out a form and your money will land in your brokerage the next working day. There aren’t normally any issues as the brokerage can see that the money is coming from your personal bank account in your name.

Due to anti money laundering policies, brokerages often must see that the money is being transferred in your name, otherwise they will return it to you. This is due to financial institutions’ requirement to see the origin of funds. However, you tend to pay for this efficiency and convenience with higher fees and a poor exchange rate. This method can be useful for your first transfer to ‘test the waters’ and try out investing. It’s more important that you get started – you can always optimise as you gain more experience.

2. Revolut

I have heard mixed reviews of Revolut and haven’t personally used them myself, although it is on my to-do list to create an account and give it a go. Some people struggle with opening an account and it is not available to everyone. For UK citizens, if you have a UK address and phone number (which I believe can be changed after the initial setup) you can set up a Revolut UK account. For citizens of the European Economic Area plus Australia, Canada, Singapore, Switzerland, and the United States, you can also open an account in their Lithuania faction.

Once you have an account opened, you can transfer from a limited number of banks in the UAE, including HSBC, ENBD or ADCB (in the branch). If you don’t have an account with one of these banks, you can open a savings account for the purposes of Revolut transfers. Then transfer AED to AED and exchange in Revolut before sending on to Interactive Brokers (or your broker of choice) in your desired currency. Sometimes you may be charged approximately 30AED to transfer out of your UAE bank and Interactive Brokers may hold the money for a few days before you can trade.

Ensure you notify Interactive Brokers that you will be sending money from Revolut by clicking ‘Manage your Account’ then ‘Transfer Funds’ before clicking on ‘Bank Wire’. You also need to specify that you are transferring to another person in Revolut to avoid any money laundering issues.

To transfer from Revolut to Interactive Brokers or another account, you can transfer £1000 for free and after that you will be charged 0.5% unless you pay for a Premium account. At the time of writing, the cost of a Premium account is £6.99 a month or £72 a year. If you wish to make regular payments, it may be worth paying this membership cost to avoid the exchange fees.

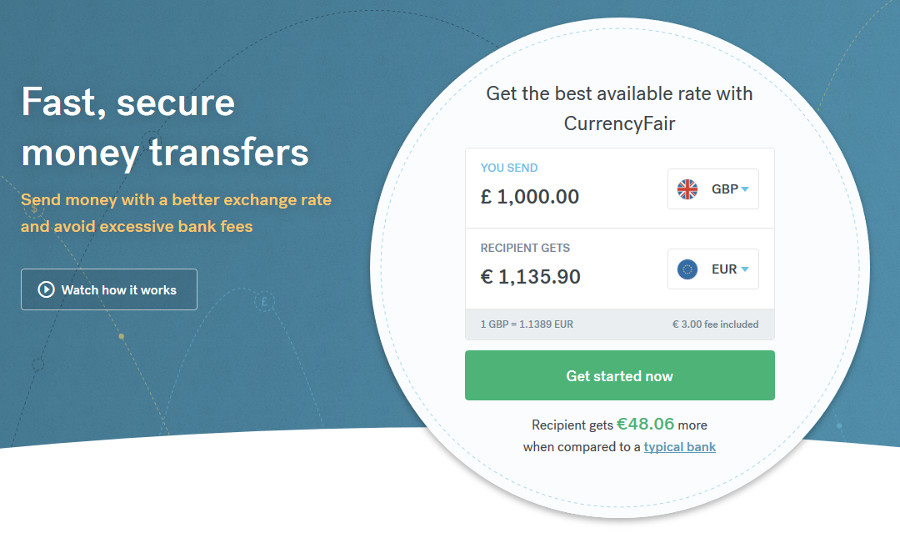

CurrencyFair on the other hand does have competitive rates. They charge a 0.45% markup on mid-market rates for FOREX and a flat fee of just €3 (or currency equivalent). However, as CurrencyFair is based in Ireland, some people have had issues transferring money from the UAE and, despite it being an AED-to-AED transfer, found themselves with an international transfer fee. It also can be a lengthy process and takes up to 10 days to complete. On the whole, this is a low-cost transfer option, but again not available to all nationalities (the full list is here).

4. Wall Street Exchange and Lulu Exchange

Both of these exchange houses have identical costs, but with Lulu Exchange, you don’t have to visit a branch every time you complete a transfer as you do with Wall Street Exchange. These two have great FX rates, particularly for exchanging to USD. For fluctuating currencies, the spread can range from 0.1%-1%. If you wish to exchange AED for USD, Lulu and Wall Street offer 3.6735 and a fixed fee of 157.5AED.

The service is fast, efficient and reliable too – usually the money lands in its destination within 24 hours. There are no intermediary charges or other hidden fees and only one transaction required by you – transfer the money locally to Lulu or Wall Street and they will remit to Interactive Brokers (or wherever you like) on your behalf.

There is no perfect or ideal way to make international transfers for every single person. The market is ever-changing and competitive and what works for one person might not work for you. Some people want the lowest cost option and are willing to put in multiple steps manually to avoid fees. Others want convenience and efficiency.

Personally, I find Lulu Exchange suits me the best. I send my contact at Lulu Exchange a WhatsApp message when I am ready to transfer. He acknowledges my message and sends me a receipt. I set up my bank wire notification on Interactive Brokers then transfer the money to Lulu Exchange – FAB to FAB. They then remit the money to Interactive Brokers in the next 24 hours and the receipt breaks down the exact charges and exchange rate.

I like the fact that it is reasonably priced and convenient. I also wait until I have at least $6000 to transfer so that the fees represent a lower percentage of my transfer. If you would like the name and number of my contact in Lulu Exchange, get in touch and I will share the information with you

Options for international money transfer

It is also worth noting that the methods I have outlined are not exhaustive – there are many exchange houses, banks and methods available in the UAE and Middle East. I would recommend that you use a reputable financial institution, regulated by the Central Bank.

Exchange houses can find themselves caught up in controversy and money laundering scams and can be shut down rather swiftly. Smaller, unregulated institutions are much more likely to find themselves in this situation, but larger exchange houses can fall victim too. A few years ago, a large exchange house halted business abruptly and if you happened to be midway through a transfer, it took a long time for funds to be returned. If in doubt, visit the SimplyFI Facebook group for a wealth of information and experience on this topic.

Finally, remember that your money is better in the market so don’t let the process of transferring it hold you up. Try different methods until you find the one that suits you. For the methods listed above, they all have customer services that you can contact and if something goes wrong along the way, your money will be returned to you. Alternatively, you can invest with a robo-advisor such as Stashaway to avoid the international exchange fees. You may still have to transfer money for other reasons, but possibly not as often as if you use an international brokerage to purchase your investments.

What’s your experience with international money transfer? Comment below with your preferred method and why.