You probably left your home country to work as an expat for a higher salary, better employment package and quality of life and to experience a new culture. However, mental health concerns such as loneliness and homesickness quickly led to behaviour that increases the likelihood of financial stress. You spend more, and you aren’t sure how to invest and save for the future while living abroad anyway. There are so many scams you decided to put that off until you return home.

But niggling worries at the back of your mind – I should be saving more, and I should really be contributing to a pension – can lead to financial stress, depression, and anxiety, meaning that expats can be more prone to money-related mental health issues.

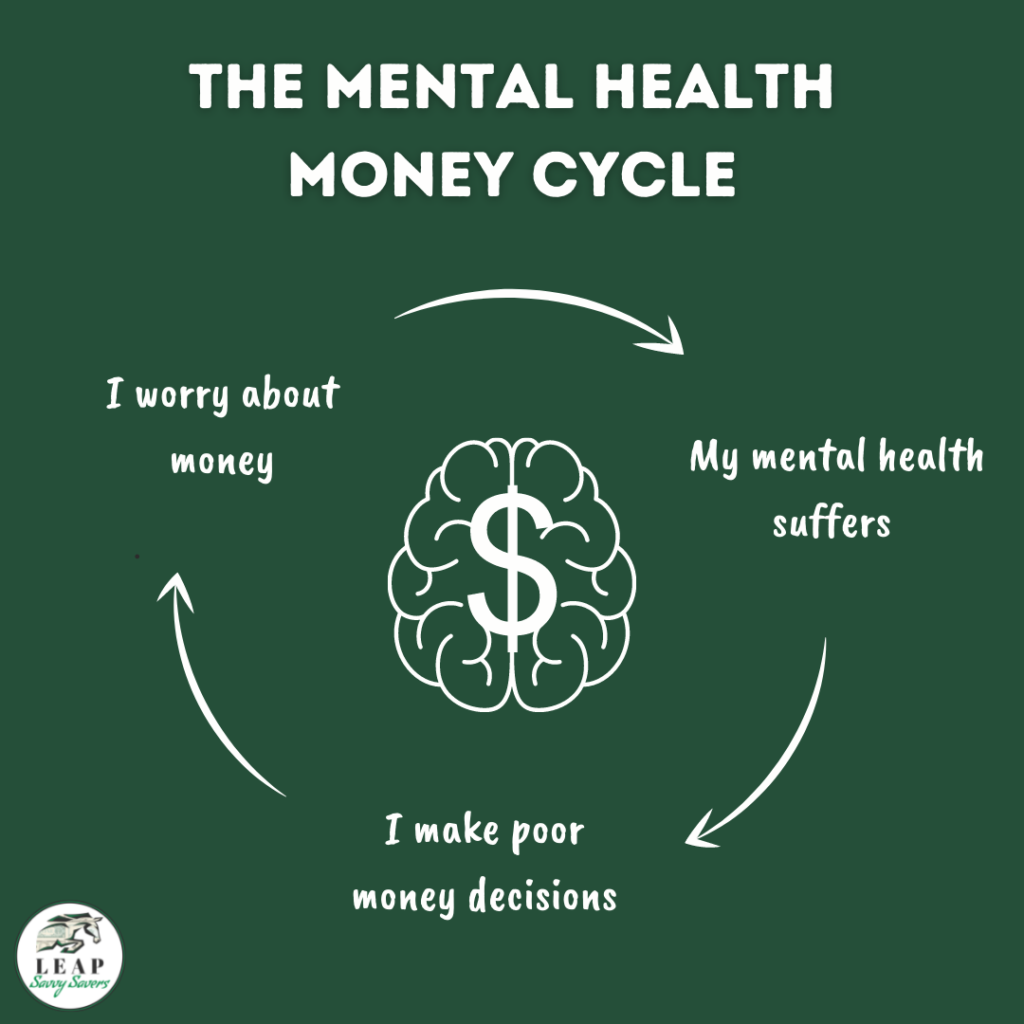

The link between money and mental health

The link between money and mental health is a hot topic, and for good reason. According to the Money and Mental Health Institute, almost half of people with consumer debt also struggle with mental health issues. It leads to a negative cycle – mental health issues make it more difficult to earn, manage and save money and the resulting stress causes deepening depression.

People with common mental health problems may experience barriers to money management that simply ‘creating a budget’ might not fix, such as poor memory or impulsivity issues. On the other hand, severe and chronic money worries can cause depression and anxiety, which leaks into all areas of an individual’s life.

Why are expats more likely to experience financial stress?

For expats, added factors such as loneliness, isolation and homesickness can amplify these problems. And it is a problem not discussed enough. It seems that leading an ‘exciting’ expat lifestyle in a foreign country is assumed to provide immunity for all these issues. But on the contrary, the lack of a support network and financial knowledge in that country can exacerbate financial stress and mental health concerns.

The statistics support my theory that many expats are not financially savvy. Global consultancy firm Mercer report that 45% of expat employees in the UAE either have not planned for a sufficient retirement or plan to work post-traditional retirement age to compensate for their lack of savings. A whopping 99% expressed the need for better savings and investment options as expats.

It’s one thing to earn a tax-free salary; it’s quite another to know what to do with that money. Corroborating this, leading financial news provider Zawya found that half of UAE expats are saving less than 5% of their income. When we marry these statistics with the William Russell findings that twice as many expats reported feeling trapped or depressed when compared to people working in their home countries and twice as many expats experienced high levels of anxiety, a tentative link may be forged.

Seeking help for mental health concerns can be more challenging than in one’s home country too – treatment may not be covered by insurance and could be costly and difficult to seek out.

Here are three financial red flags which could contribute to mental health concerns for expats. This is by no means an exhaustive list, and any time you feel low for a more than a few days or anxious to the point that it begins affecting your daily life, you should seek out medical treatment. This is simply for the purposes of raising awareness and offering tips for expats but does not replace professional medical advice in any way.

1. Impulsive purchases or overspending

When expats leave their home countries, they may have expectations that the lifestyle in the foreign country will solve all their problems. When the reality falls short of the expectations, the result can be increased depression or anxiety. There can be a pressure to ‘enjoy the lifestyle’ in the expat country and forge friendships, meaning an increase in spending.

A constant feeling of being on holiday mixed with easily available credit can often mean expats find themselves in quickly escalating credit card debt. Increased feelings of isolation, loneliness and homesickness can result in impulsive spending as a way of dealing with or escaping from those feelings. This contradictorily heightens the feeling of being trapped as you have to stay until the debt is paid off.

Perpetuating feelings of fear, negativity and anxiety is the challenge you may face in seeking support if you find yourself in spiralling debt. There is not much by way of financial assistance once you’re in a difficult financial situation in the UAE. It is slowly changing, and the Government is planning on bringing in financial aid policies for expats, but at the time of writing, it will be some time before those sorts of options are available.

2. Living in a doctor's waiting room

This red flag is the polar opposite to the experience of the individual in scenario one. Not all expats have the same experience, and a range of issues could lead to a variety of mental health concerns.

Some expats feel a great deal of pressure to save for the future and make the most of their tax-free salaries while they are away from their home countries. If this is you, you may have started forfeiting the present day to save for the future. If you do this too much, you develop a feeling that you are living in a doctor’s waiting room, just constantly preparing for your ‘real life at home’ to start up again.

Sacrificing too much joy in the now for the future can lead to high levels of anxiety and resentment towards people ‘living their best lives’. Situations out of your control such as the rising cost of living and the global pandemic may also throw a spanner in your plans, resulting in even more anxiety.

3. Running out on retirement

You moved abroad, you got settled in your job and you decided to sort your financial house out. You don’t know how pensions and investments work in your expat country, so you met with a financial advisor – someone with the expertise that you lack. They set you up with a savings plan – this is in lieu of pensions in your home country, and you invest a fixed amount each month and in 25 years you be able to retire. All you had to do was assign a few papers. Sorted. Or not.

What many people realise too late is that these savings plans charge so much in fees that the first 18 months of payments often go solely to fees. They charge up to 4-5% in fees per year, which might not seem like a lot, but over decades can be 100s of thousands of dollars. If you pay 4% in fees, and the stock market returns 8%, you are losing out on 50% of your profits, as shown by the orange ‘active managers’ line in the chart below. Not to mention the 1.5% credit card fee and 0.75% mirror fund charge to invest in a fake fund! This on top of a surrender fee if you wish to exit early (which the vast majority of people do) is enough to put people off investing for life.

If you have signed up to one of these long-term savings plans, there is hope. Check out Steve Cronin at Dead Simple Saving for more support. However, it can take a toll on your mental health to be scammed by these confident, slick advisors. You could lose confidence in your money management skills, feel depressed about the money lost to the scheme and fear investing again.

This could lead to feelings of depression, anxiety, stress, worry about the future and being duped again as well as the perception that you are now ‘behind’ on retirement planning. This is not true – you absolutely can recover and get back on track, but it doesn’t negate the feelings that bad investments can bring, which are completely valid.

What can I do if I have money-related stress or mental health concerns?

First and foremost, seek professional medical advice if your mental health has started to impact your daily actions. If you are experiencing changes in sleep, weight gain or loss, or feelings of hopelessness or despair, visit a doctor and explain your situation.

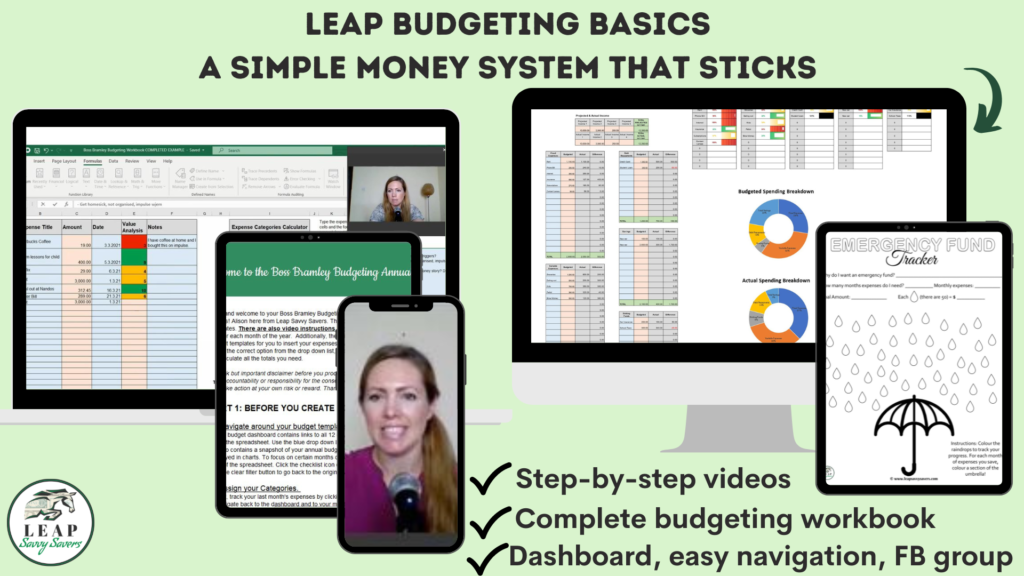

If you’re feeling run-down, resentful or burnt out over money issues, it’s perfectly normal, and there are things you can do to improve your situation. No matter whether you’re 5 years into a failing savings plan or have managed to accrue Dh30,000 of credit card debt, just making a plan to start moving in the right direction and getting on track can do wonders for your mental health. Start by creating a realistic budget and setting financial goals.

Try to connect with other people. Make friends and talk to other expats (whilst spending within your budget!) with the same interests and hobbies as you. It might be cathartic to realise that you aren’t alone and other people are experiencing similar feelings (you don’t need to spill your life story but sharing feelings of homesickness might help you connect).

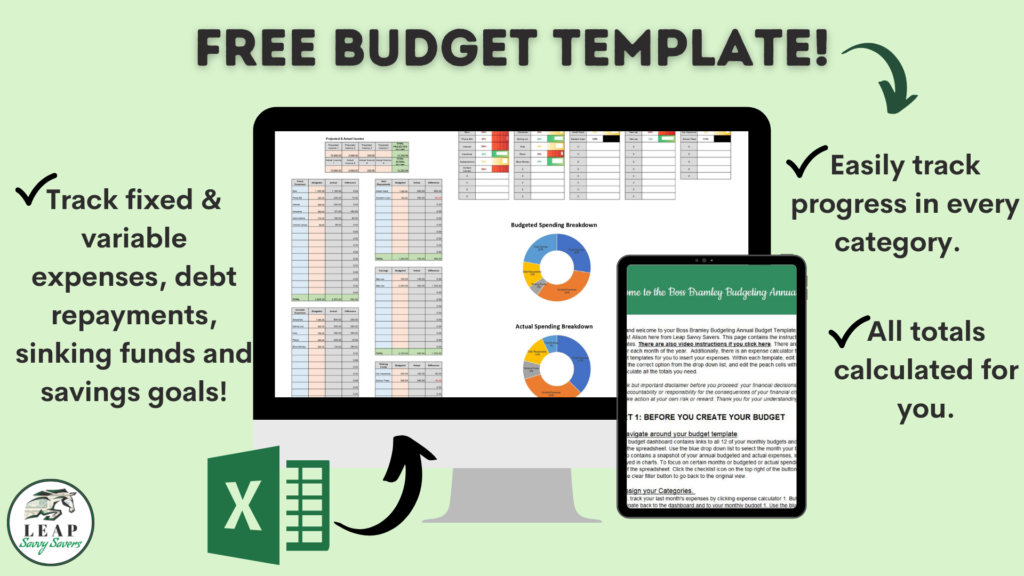

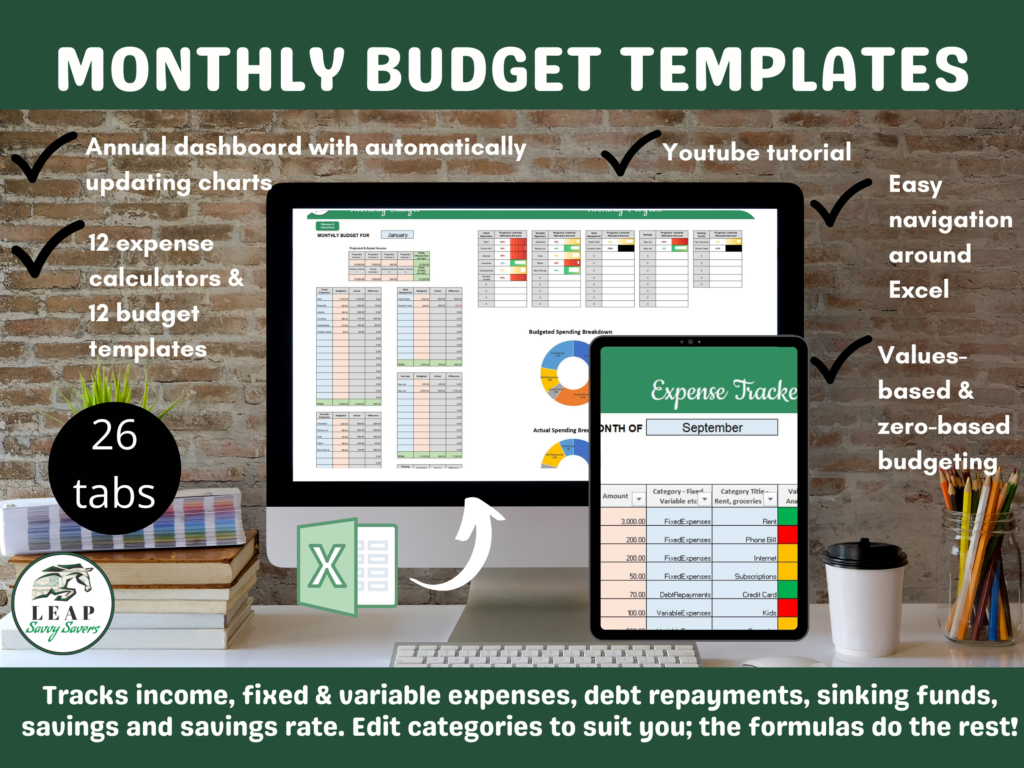

Build mental health into your budget. I have a ready-made budget template for you to use which monitors your income and expenses and uses colourful charts to track your progress towards your goals. Use it to plug in mental health activities to your monthly spending, whether that is therapy, a gym membership, or a spa day.

Finally, educate yourself on saving, budgeting and investing as an expat. Equip yourself with knowledge so that you can build financial security and wealth while living abroad. It might not solve all your mental health concerns, but it can help alleviate some money stress and financial worries. Finding your balance between living in the now and preparing for the future is the key to getting the expat life right.