Savings rate is a fairly straightforward metric to calculate and track. It is essentially just your total income minus your total expenditure in any given pay cycle, month, year, or other timeframe of your choice. This is, in my opinion, the best indicator of your financial health. Your savings rate reveals how much disposable income remains once you have done all your spending. This can be used to predict and make strides towards retirement; but what’s a good savings rate to retire early?

How do I calculate my savings rate?

To calculate your monthly savings rate, simply take your income and minus your expenses. For example:

The person in this example has 33% of their paycheque left over once they have paid their bills. You can work it out as an individual, couple or household. To add more people, just total all your income and your expenses and complete the calculation.

In terms of what to include in the expenses side of the equation, you should decide which items you consider ‘savings’ and which you define as ‘expenses’ before you do the calculation. For example, I include my contributions to my sinking funds on the expenses side and money put towards savings goals into the ‘savings’ side.

Even though technically I’m saving into my sinking funds, that money is already earmarked to serve a spending purpose in the near future, such as flights, visa costs, school fees or medical bills. Thus, I allocate my sinking funds contributions to expenses. I don’t include the spending I do out of the sinking funds in the equation as they are spread over the year.

If I included those large expenses plus the sinking funds contributions, it is a double up of expenses and inaccurate. For example, if I spend Dh20,000 on a flight in July, I don’t include that expense in my monthly savings rate calculation. Instead, I enter the Dh1700 I save towards flights every month. Of course, this only works if you regularly save towards your sinking funds. If you don’t, you will need to include all expenses, big and small. I give detailed and visual examples of exactly how to do this in my Leap Budgeting Basics course – the simple money system that sticks.

Do I use my gross or net income?

There are a few ways to calculate your savings rate. The first method is to take your gross income and minus the deductions, such as tax or health insurance, as expenses. If your employer contributes to a pension on your behalf, you can input this onto the savings side of the equation.

The second way is to base your calculation on your net income and expenses, as outlined in the example above. Don’t factor in your tax and pension etc. and simply track the money you have control over spending.

I go into detail and give examples of working out your savings rate using different factors in my Leap Budgeting Basics course. However you choose to calculate your savings rate, as long as you’re consistent with what you factor into the formula, you will have an accurate measure of disposable income over time.

Can I have a negative savings rate?

If you have a negative savings rate, it means that you are living beyond your means. This is how you get into debt. For example:

The person in this example is spending Dh2,000 more than their Dh15,000 income. That means that they are overspending by 13% of their total income. Even what may appear to be a ‘negligible overspend’ is a substantial wedge of your income if you work it out as a percentage. If you’re spending more than you’re bringing in, you either have to draw on savings or debt to cover the excess. This requires an urgent assessment of your expenses to see what you can cut or reduce to ensure that your savings rate is a positive number.

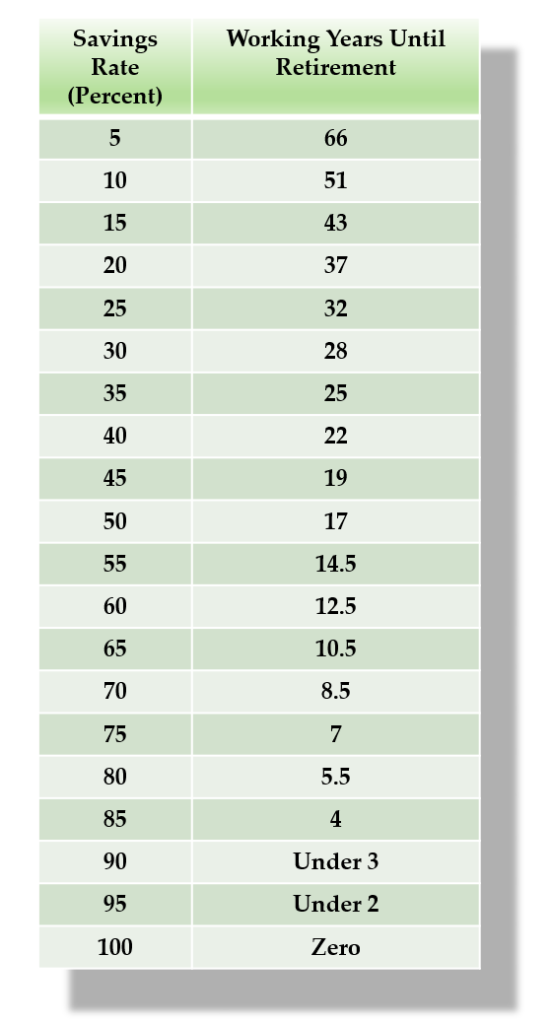

Most financial planners will advise you to save at least 10% of your income towards retirement. Really, it’s up to you – how much disposable income do you want to have? Ideally, you should have at least some level of buffer to protect your finances in case of unexpected expenses, emergencies, or rises in costs. Living paycheque to paycheque is a sure-fire way to sleepless nights and stress.

My personal goal is 50% of my income averaged over the year, with an aspiration of 60%. Bringing up two children in a high-cost-of-living area, this is challenging enough that it keeps me on top of my finances, but still allows for a standard of living that we as a family enjoy. Finding your ideal savings rate will be personal to your circumstances, but I recommend that your goal be a little challenging without compromising your quality of life.

The higher your savings rate, the larger your contributions to your retirement/investment accounts so the faster compound interest will work its magic for you.

The lower your living costs, the less of a retirement ‘pot’ you need to draw from to cover your living expenses

How can I improve my savings rate?

To improve your savings rate, you have two levers to pull: reduce expenses or increase income. Reducing expenses can include the following actions:

Alternatively, you can increase your income by training for a promotion, applying for different jobs or starting a side hustle.

What's the best metric in personal finance?

You can track a range of numbers in personal finance – net worth, investment returns, return on investment, dividends, income, expenses and so on. So, why is savings rate so special? It is different to most of these other measures in that it is the metric that is MOST IN YOUR CONTROL.

Nothing in this world is completely within your control. But you’re going to be disappointed fast if you track returns on your investments or net worth. These numbers can swing wildly depending on market and economic conditions and you’ll be more susceptible to emotional selling when the market is down.

You’ll feel much more satisfied tracking your own actions. You’re the one who is accountable to your savings rate. Of course, factors such as inflation play into your savings rate. That’s where you can make adjustments though – if you really want to maintain your savings rate, you will find a way of creating an additional stream of income or cutting an unnecessary expense.

You could track your income or your expenses independently; however, one doesn’t mean much without the other. If a person is making $500k a year, you might think, wow, they’re doing really well. But if they’re spending $600k a year, they’re situation is unsustainable and probably pretty stressful.

Your savings rate tells you so many things about your financial health and is easy to track – it doesn’t take me longer than one hour a month using my spreadsheet to calculate this significant number, crucial to all savvy savers’ journeys. When asking yourself ‘what’s a good savings rate to retire early?’ make sure you are also asking yourself if you are creating a life you can love now as well.