Struggling to manage money? Want to know where all your money went? You will hear the same advice almost every time: create a budget. But which budgeting method is best? And how do you create a budget that you will actually stick to and will help you make the most of your money?

There’s a reason it’s called ‘personal finance’ – there isn’t one way to manage your money. Only around 2 in 5 individuals create and follow a budget, but all successful businesses have a budget, because they know it is the most effective way to manage money.

Chances are you’ve tried to budget in the past but either not stuck to it or not updated it and gradually fizzled out. If that sounds like you, try a few different methods until you find the one that you can maintain for the long-term. It has to suit your unique circumstances; be simple enough that you can keep going whatever is going on in your life but complex enough that it encompasses all your various spending habits and income streams.

I have 3 golden budgeting rules despite the method:

Here are 5 simple budgeting methods to try. Each has their strengths and drawbacks and no one method is more or less effective than another – it’s which one suits your circumstances best.

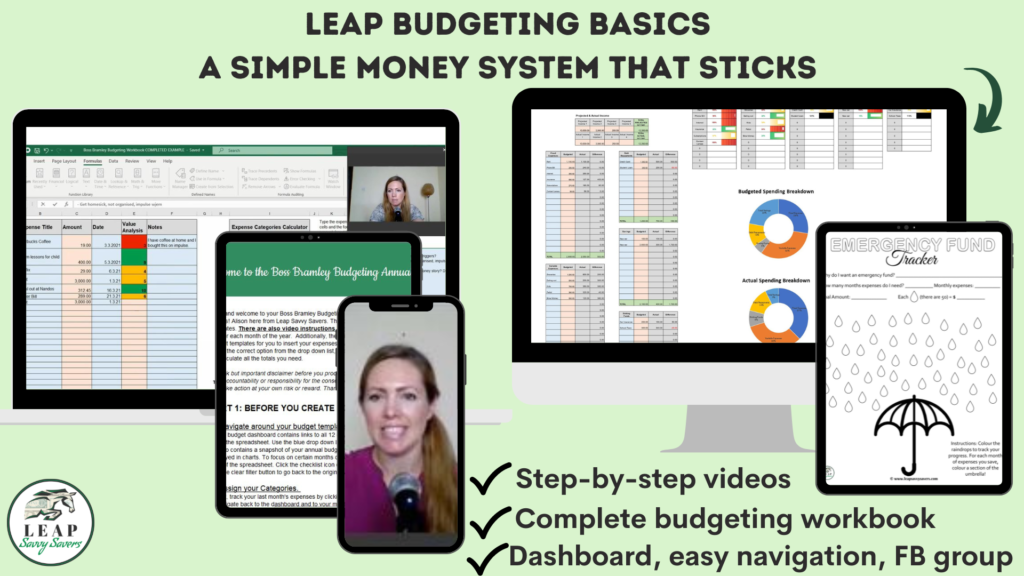

1. Zero-based budgeting

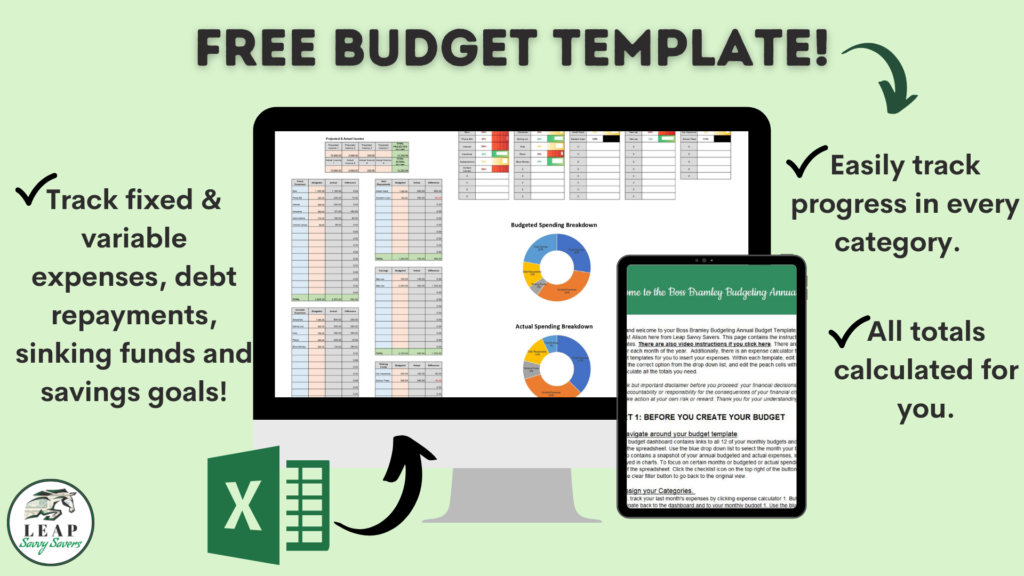

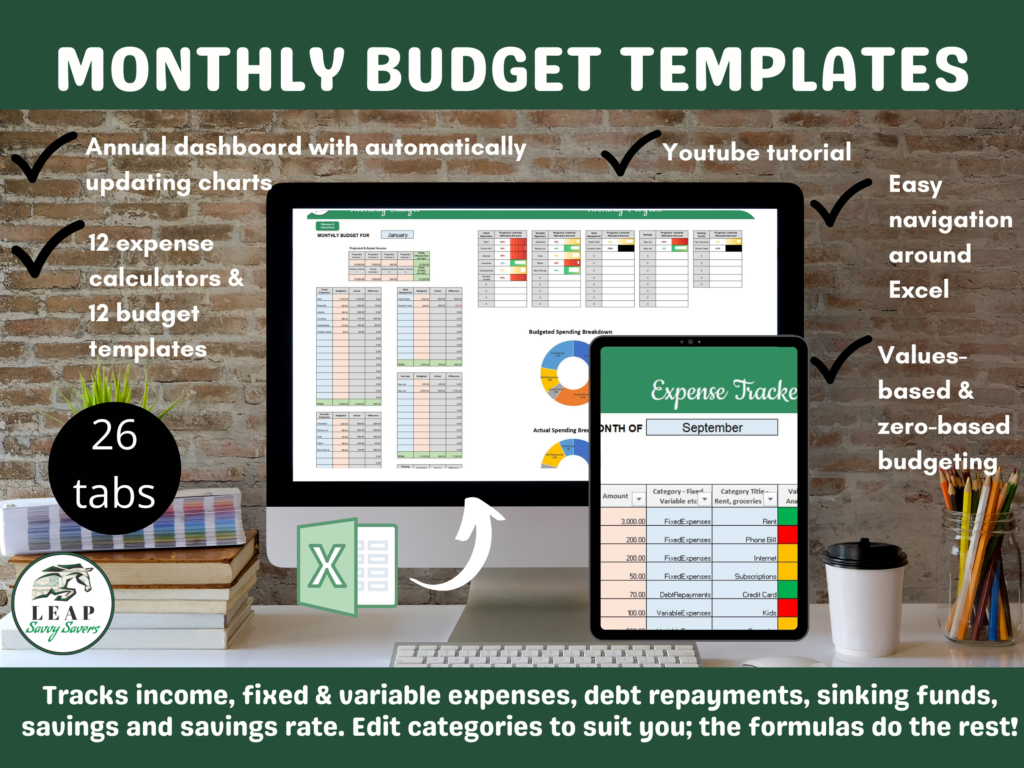

My favourite method – give every dirham a duty. The zero-based budgeting method works by assigning every dollar/dirham/pound you earn a ‘job’ to do before the money hits your account. This works best for people with regular income streams, such as a fixed monthly salary. It’s also very effective for people who are paying down debt or have savings goals that they are prioritizing. I have used this method for over 3 years now to maintain a 50% minimum savings rate.

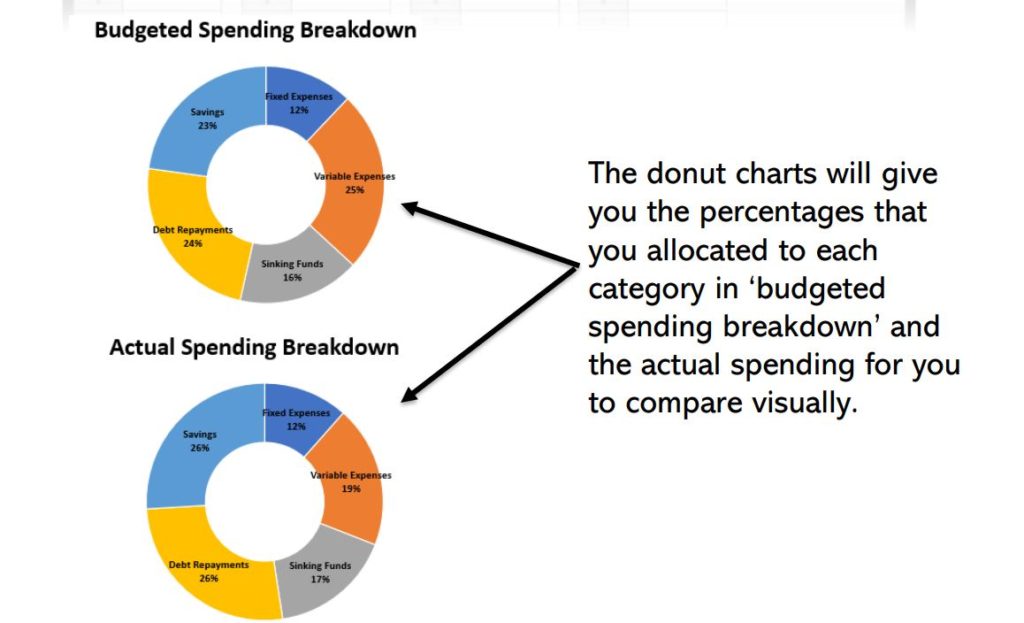

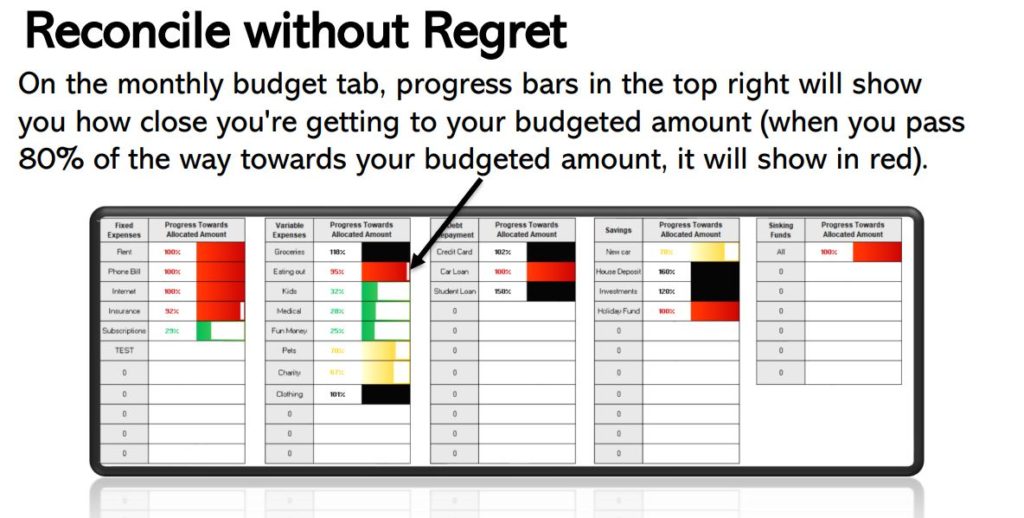

This spreadsheet templateautomatically calculates the totals for you to ensure you aren’t under or over budget. You simply input your expected income at the top of the spreadsheet. Then, once you have assigned money for your fixed bills, debt repayments and savings, you can allocate money for variable expenses, such as dining out, until you reach 0, hence zero-based budgeting. Before your income even hits your account, you know how much you have to spend in each category.

This works well in conjunction with the envelope method (see below) as once you have assigned amounts to categories, you simply stuff your cash envelopes with the correct amounts and go about your life. If you’re not into cash and prefer to spend on a credit card (whilst ensuring it is paid in full before any charges are incurred), simply use my spreadsheet to track your actual spending next to your budgeted allocations. Towards the end of the month, reconcile your budget by calculating how much you spent in comparison with your budgeted amounts in order to plan for the following month.

2. Cash Envelope method

This method is great for people who naturally overspend and lack the discipline to use a credit card responsibly. If you’ve been in and out of credit card debt and often make impulse purchases that you wind up regretting, cash envelopes could be for you. Recognising this tendency in yourself and seeking a method to support your money management is commendable.

The method is fairly simple – once you have decided how much you will spend on each category for the week or month, depending on how often you are paid, stuff your cash envelopes with the amount you want to spend. Go out and about without your cards with the attitude that once the money is spent, it’s spent. This can help you develop the discipline required to use a different budgeting method. It’s not as effective if you are someone who’s already quite frugal and can benefit from the points and rewards associated with credit cards (when used responsibly and paid in full).

3. The 50/30/20 budget method

Many finance experts call this method the 50/30/20 method, but I prefer the Percentage Plan. Another simple money management technique in which you allocate a percentage of your income to fixed expenses such as rent, utilities and groceries (50%), variable expenses such as dining out and entertainment (30%) and savings and investments (20%). This could be effective if you don’t have a complex financial picture and want to spend very little time on your money.

Instead of prescribing percentages though, I think it would be more beneficial to assess your personal situation to see what percentage of your income is realistic for you to put towards fixed expenses, variable expenses and savings. For example, someone who is on a modest salary and living in a high cost of living area may have to spend a larger portion of their income on necessary living expenses. However, if you want to ensure you are allocating a certain amount to retirement (such as 20%), this method might work for you. The key is figuring out what lifestyle you want to live and your goals and making the percentages work for you, rather than trying to fit your life around some arbitrary figures that someone on the internet prescribed.

Once you get paid, simply transfer the percentages to different accounts and spend from there. One way this would be effective is to ascertain at the start what you currently spend on different categories and evaluate whether you’re happy with it. If you are spending more than 50% of your income on housing, you may want to consider applying for a promotion or moving to a lower cost of living area, if you feel ‘trapped’ by this expense. On the other hand, if you are really happy in the area you are living in, spending a large portion of your income on rent or mortgage might be worth it for you. It all depends on your situation.

4. The Pay-yourself-first budget

This method works well for people who wish to aggressively save for financial independence or pay down debt rapidly. With this budgeting strategy, you simply decide how much you want to save and use the rest of your income to live on.

For example, if you have worked out that you want to invest $2500 per month, then that is the first thing you do when you get paid and you are forced to live on the rest and make it work.

This could be effective if you don’t have dependents or a lot of bills or liabilities but could cause issues if you can’t pay your bills. I’m all for increasing your savings rate, but I advocate for making sure all your bills are paid on time to avoid fees and high interest debt.

5. The automatic budget

This is also called the ‘no budget’ method and can work for people who feel extremely restricted by traditional budgeting methods. It can also work for naturally frugal people who have a tendency to restrict their own spending at the expense of their own happiness or fulfilling their own basic needs.

If you use the automatic budget, you automate as many of your expenses and bills that you can and then don’t allocate set amounts for variable categories but simply track what you spend. It works like a backwards budget where as long as your bills are paid, you go with the flow and track what you have spent. You might make mental notes about which areas you spent a little too much or too little in as you track, but other than that, you freely spend. I would not adopt this method unless you are naturally frugal and are not at risk of spending more than you earn.

For a person using this method, I would recommend having money set aside in an emergency fund and for any sinking funds (large, planned expenses) that you have coming up in the next 6-12 months, so these don’t catch you out.

This method might be useful for someone who has already achieved financial independence or ‘coast FI’ (a state whereby you have enough invested that when you reach the age you wish to stop working you will have enough money to passively live off for your retirement) who doesn’t have to focus too heavily on saving and investing.

Whichever budgeting method suits your circumstances, make sure it serves you to live the life you want and spend money on what brings you joy and cut the rest. If you have debt that you’re struggling to pay off or you can’t seem to stick to a budget, check out my online course or pop me an email to set up a coaching session. I can provide you with a roadmap to fix your finances and a clear step-by-step guide to managing your money.