17 August, 2021Apply / Invest / Learn / PersistA couple of years into living and working in the UAE, I had met and married my husband and was pregnant with my first baby. The original plan to ‘work for 2 years, save enough money for a house deposit and move back to the UK’ was clearly evolving rapidly. I had a lot going on – I was newly married, studying for my master’s degree, working full time as a teacher and pregnant with my first baby. So, money, and saving for retirement especially, was not at the forefront of my mind.

However, I did have a niggling voice in the back of my mind telling me that I was missing out on paying into a pension by not working in the UK. The benefits of earning a tax-free salary come at a cost – you don’t get to pay into a pension. Around this time, I was discussing this very issue with a friend over coffee, and she explained that she put money into a savings plan, the equivalent of contributing to a pension in the UK. She just transferred in automatically every month for 25 years and boom, sipping cocktails on the beach, here we come.

I was introduced to her advisor and after a quick meeting, signed up relatively quickly. I didn’t bother asking too many questions – I had a baby on the way, and work, and life. I was busy. This was a financial advisor and they’re qualified so they know what they’re doing, right? WRONG! Looking back at my actions and priorities then, I could be talking about a different person.

I willingly handed my money over to someone without really doing research into the fees, the investments, none of it. I was told that the fees were 1% (lies!) and I thought, 1%, that’s hardly anything. WRONG AGAIN! A small investment of money and time in ‘Millionaire Expat’ would have informed me that the fees on my portfolio, upwards of 4-6%, would cost me hundreds of thousands of dollars; but alas, I was distracted. I was such an easy customer; the advisor must have been on cloud nine. She barely had to convince me into this money heist.

Fast-forward a couple of years and I did do a Google search, and read books, and listened to podcasts, and read blogs. And cried. But I didn’t dwell too long – I got out (incurring a huge penalty and losing most of the money I had contributed) and started investing intelligently. I’m now on the path to financial independence – investing regularly, making smart choices with my money and learning continuously.

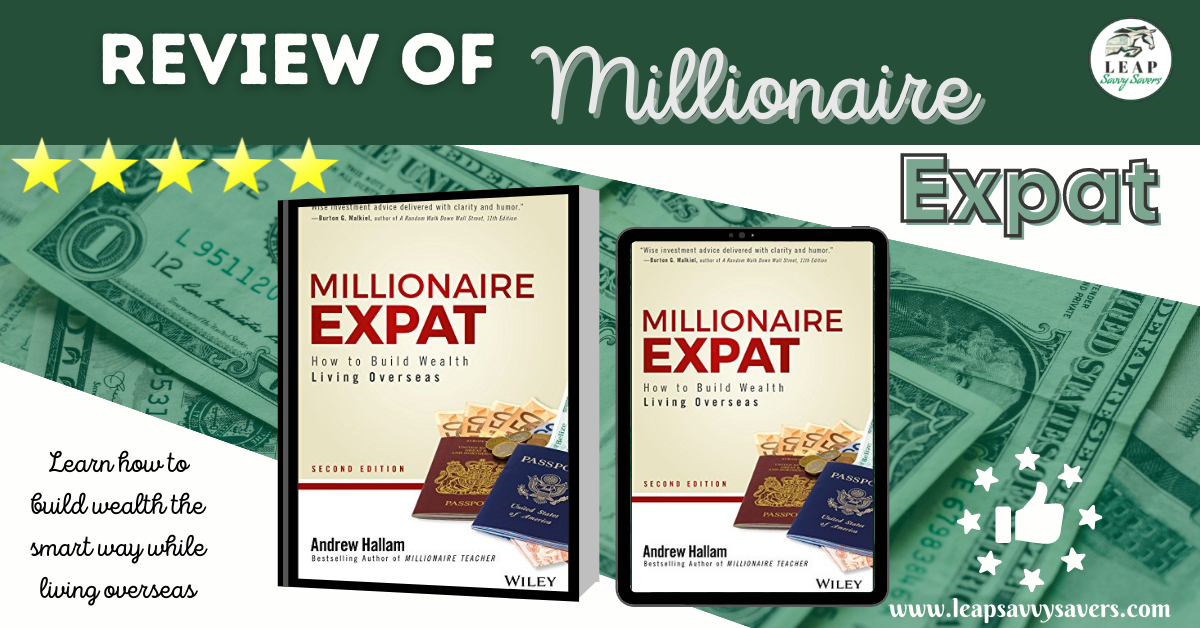

One of the books that had a massive impact on my journey was ‘Millionaire Expat’ by Andrew Hallam. The book appealed to me as Andrew Hallam built his investment portfolio on a teacher’s salary. As a teacher myself, I know that, even in a tax-free country, a teacher’s salary is by no means Lamborghini territory; its barely even ‘new car’ worthy. Hallam proves that anyone can build an investment portfolio, even people on relatively small salaries. Wow. Hope for the little guy.

The world of investing and the stock market can be daunting and confusing for a ‘regular’ person, whose job has nothing to do with the finance industry. I just thought of investing as an extremely risky business, and the stock market as a place where people like me went to lose their money. It was only the bigwigs on Wall Street that earned money from the stock market, right? WRONG AGAIN! Andrew Hallam expertly explains this potentially confusing topic in easily digestible and relatable terms so that you and I, the ‘regular’ people, have a chance of understanding it.

The humorous analogies to Star Wars, fighting escalators, roast beef and many others are underpinned with facts gleaned from studies and research. As well as setting out a clear plan for different nationalities (there are sections in the book dedicated to British, American, Canadian, Asian, Irish, Australian, South African and South American expats as well as investors from New Zealand), Hallam answers all the burning questions you may have about this all-important topic in an informative yet entertaining way.

Here are 3 key lessons I took from the book:

Don’t time the market. When people get a taste of the stock market, especially if they earn returns on their money, their ego can take control and they may think they can outsmart the market to earn more. Quoting from experts like John Bogle and Warren Buffett and providing helpful visual charts showing investors’ returns in comparison to the stock market returns (3.98% to 10.16% from 1986-2016), Hallam sets about proving that nobody can successfully predict the future. A *boring* strategy of investing every single month (or as often as one can) no matter the circumstances or price, is your best shot at building a successful investment portfolio.

It’s important to invest in government bonds (loans to governments rather than to companies) as well as stocks. Now bonds can be less exciting than stocks. They don’t tend to earn huge rates of return and interest rates are fixed (usually around 3% so you barely beat inflation). The less bonds you have in your portfolio, in theory, the faster it will grow. But it will be exposed to higher volatility. Bonds are not likely to drop 50% if the stock market does, so if you have some in your portfolio, your investments aren’t going to drop by 50% either. In case you aren’t convinced, Hallam proves through factual data that a portfolio of purely stocks doesn’t necessarily beat a portfolio comprising stocks and bonds.

Decide on your long-term strategy and stick to it. Using practical examples and figures, Hallam explains why leaning in to ‘the next big thing’ is more likely to be a disaster than a dazzler. Stock pickers and people trading regularly were found to underperform the overall market by 4%-13%.

My signed copy of ‘Millionaire Expat’.

Buying this book might be one of the greatest things you can do for your future self and your family. Having met and listened to Andrew Hallam speak several times (as well as having him sign my book – pictured above), I can honestly say that this is a book review close to my heart. Investing less than a hundred dirhams in this book could (or should I say WILL if you take action) result in you saving hundreds of thousands and making hundreds of thousands of dollars (millions over your investing lifetime). Now that’s a return on investment that I can get onboard with!

This page may contain affiliate links, which means that if you click a link and make a purchase, I might make a small commission at no extra charge to you. Click here to read the full disclosure and privacy policy.

Buy the book here!

Millionaire Expat: How To Build Wealth Living Overseas

Buy now!

Buy the kindle version here!

Millionaire Expat: How To Build Wealth Living Overseas

Buy now! [...]

Read more...

7 August, 2021Apply / Learn / PersistSometime in August, most parents start thinking about back-to-school preparation. Some look forward to school commencing with excitement after a long summer entertaining the offspring; others may feel slight (or major!) trepidation at the thought of the chaotic mornings, extracurricular clubs and homework starting up again. Whichever camp you fall into, some back-to-school shopping will most likely be involved.

Parents want the best for their children and companies know this, thus school items tend to be a tad on the expensive side (to put it mildly!). Keeping up with the Joneses is not limited to the large house and luxury car. School bags, shoes and even stationery can be subject to school gate comparison. This year the start of school may be particularly nerve-wracking due to it being the first time back full-time for many children since the start of the pandemic, leading to parents spending more to help their child to feel secure and prepared. I get it. I want my children to be prepared too. But there are ways to prepare your mini-me for heading back to the books without blowing the budget and still prepare them for the best start to the school year.

1. Take inventory of what you already have

During the summer, I take out all the previous year’s equipment and uniform and try it on. If something fits well enough and is in good enough condition to see out another school year, then it continues to serve its purpose. I also ‘shop my home’ for stationery items and decent water bottles lurking in the backs of cupboards. I can often find most stationery equipment that my children would need so can add it to the inventory list.

2. Write a Specific list

Decide before you go out shopping exactly how many of each item you will need. For example, how many sets of Physical Education uniform do you need? How often will your child have P.E.? How many times a week can you feasibly wash the uniform? It might be worth putting a note in your calendar to contact the school in June to check you are purchasing the appropriate things. I usually have 3 sets of main uniform pieces and 2 sets of P.E. kit, but this will depend on your situation. Make sure you remember to make a list of all equipment, such as socks, a hat (if you are in a hotter climate), specialised items such as a scientific calculator or protractor, a lunchbox and a swim kit.

3. Buy quality items (especially shoes and bag)!

I’m all about penny-pinching, but when it comes to school equipment, the wear and tear is going to test the stuff to the max. I will always splurge for quality footwear to support my growing child, and a sturdy bag, lunch box and water bottle. I don’t care so much about brands, more quality and durability.

I have a Bento lunchbox for my son and find it to be reliable, leakproof and keeps food fresh. It was a tad on the expensive side, but I’m sure will last several school years.

You may have a personal favourite brand of school shoes – mine is Skechers, but Clarks is well reputed to have high quality footwear. It is super important to get a proper fitted shoe to support child development, so I think heading out to the shops rather than online shopping is a must for footwear.

When purchasing a water bottle, I think about ease of use for younger children, and ease of cleaning. I often find that lids can be difficult to dismantle and clean and thus mould starts forming around the mouthpiece. I find CamelBak to be the best water bottle brand – reliable and spill proof. It’s definitely pricey but could last for several school years so be a saving in the long run.

A sturdy school bag is a must, especially now that a lot of schools are allowing children to bring their own device, meaning that they potentially have books, equipment, lunch and a laptop. Eeek. A comfortable bag is a must. L.Bean and State Kane are highly reputable brands for resilient and ergonomic school bags.

4. Shop around for the best prices

Schedule some time to browse for prices in your area well before school starts. Have a look at online and brick and mortar options as well as reviews. I recommend doing research on your own first to get the lay of the land, then, depending on the age of your child, you could get them to browse your ‘top 3’ and make them feel that they are making the decision.

5. Set a hard-limit budget!

Once you’ve got a firm list and have shopped around, you’ll have an idea of what things will cost. Tally it up and set a budget and stick to it! The amount you settle on should be your hard limit. It’s useful to keep a budget line item of school equipment in your variable expenses category so that you can refer back to it next year and line them up to make sure you’re not heading off into Joneses territory! I have a great budgeting tool in my Etsy store to help you keep track of all expenses with ease.

Depending on the age of your child, sharing your calculations and the budget with them could be a fantastic teachable moment. You could discuss the importance of planning out spending within a budget and living within one’s means, even when the desire to spend more to look a certain way or keep up with fashion may be strong. Use it for a lesson on the negative compound interest of credit cards versus the positive compound interest of investing if your child is engaged in the conversation, particularly if they want more expensive items. Share the example below if it helps to give the visual!

6. Pick the optimal day and time to go back-to-school shopping

Don’t go on a day that you have other appointments or meetings scheduled, and don’t go hungry or tired! This is an important shopping day and requires focus and self-control for you and your child! Some people prefer to spread out the shopping; for example, uniform one day, equipment another, while others prefer to get it all done in one session. You decide what’s best for your family. For me, I like to make it a memorable day for my child, so if we have agreed on the budget and list beforehand and my child demonstrates adequate restraint, we go for coffee/juice and cake after shopping. Shopping trips are such a rarity for my family that I do try to make it an occasion if I can!

7. Shop year round for back-to-school season.

Finally, keep an eye out during the whole year for items which might be on sale at other times, such as January sales or Black Friday. Things like clothes and shoes may have to be purchased close to the start of school due to sizing, but bags, water bottles, equipment and lunchboxes may be on sale at different times of the year.

I hope these tips have given you some ideas to start this school year off with a bang while sticking to your savings goals. If you have any further recommendations for back-to-school savings or brands that you swear by, comment below. Wishing everyone (parents, teachers and students alike) a peaceful and successful school year. Happy shopping ?

Need A Bit Of Support with your finances?

If you would like to book a confidential financial accountability coaching session to help you work on your finances or stay accountable to your goals, send me an email at leapsavvysavers@gmail.com or drop me a line via the contact form and we can see if we’re a good match.

Good luck on your financial journey – congratulations on taking the leap. [...]

Read more...

12 August, 2021Learn / PersistGetting a head start with money management can make a huge difference to a person’s entire life trajectory. A lot of parents fall into the trap of thinking that giving as much financial support as possible to their children is the key to putting them out front as they begin adulting.

But what is more valuable than being given money? Being taught how to manage money. Think of all the lottery winners that go broke – having more money is not always the solution. Teaching your children how to manage small amounts of money from a young age can help give them the best start in life.

So, what’s the best way to do that? We can’t just start talking to a 5-year-old about credit scores and the stock market, right? No, not advisable. But we can start guiding them in the right direction from a young age. Here are some ideas for you to implement as early as 4-5 years old.

1. Teach them that money is, at its core, an exchange of value.

Show them that money is earned from an early age; money is exchanged for value added to the marketplace. Even if you don’t want them to feel like a job is the only option later in life, most people (even those with passive income streams) started by earning or working for the money. The person who earns money from book sales must earn that money by writing the book, just as the person who works as a waitress must earn money waiting tables at a restaurant. The result is different as one becomes royalty income and one is earned income; however, the basic premise is that all people must work or create or provide to receive money.

You want one of the first lessons to be that money is an exchange at its core – you provide value or service and get paid money, then you pay money for value or service. You can teach this by example – give them money in exchange for ‘working’. Perhaps you can pay them for doing chores or if you don’t like that idea, reading books or writing a story. If you feel that everyone in the family should do chores by necessity and you don’t want the children to think that they are entitled to payment every time they sweep a floor, you can set up a roster of basic chores for members of the household, then offer to pay them for extra work. If they go above and beyond, they receive payment. However you decide to demonstrate this, plan it out before posing the idea to your children, so the boundaries are clear.

2. Separate money into 3 clear jars.

When they have earned or been gifted money, change notes into smaller denominations and ask them to split the money between 3 jars, labelled ‘spend’, ‘save’ and ‘give’. As much as possible give them the choice about how much will be added to each jar but guide and teach them what each means and make it clear that some money out of each ‘paycheck’ must go into each jar. Explain that the ‘spend’ jar is for satisfying immediate needs and wants, the ‘save’ jar is for future goals and buying larger things and the ‘give’ jar is to help or gift to others.

3. Show children the cost of things.

When you’re explaining the meanings of the different jars, ask them what they would like to spend the money on. Elicit a few things, preferably of different values, for example a packet of sweets, a toy car and a dollhouse.

Now you can explain that they could probably afford to buy a packet of sweets now, but they can’t afford a dollhouse yet and that is why they must earn more money next week to be able to buy it. Ask them which things from their list of wants they desire most. If it’s the cheap option, then they can buy it now. But if it’s the more expensive option, such as the dollhouse, then more saving is necessary.

Look at the prices of some dollhouses on Amazon together then count their money. Discuss how much they would have to work to buy it. You are teaching them that things cost money and hours of life exchanged too. Guide them to split their money between the jars depending on their goals. For example, if they really want to buy an expensive item, then more money should go into the ‘save’ jar.

Holding the money in clear jars can provide a great visual to see their stash of money growing as they earn it. You could also stick a chart on the wall above and colour it in as they save towards their goal. You are gently encouraging them into a saver mindset rather than a spender mindset.

4. Introduce them to investing.

You might think you have to wait until they are older to educate them about the stock market, but this isn’t the case. As a way to entice them to save more, especially if you have a natural spender, give them 1 AED for every 5 AED that they save. Of course, you can alter the amounts to suit you.

The point is that they learn about investment returns, passive income, and delayed gratification. You don’t have to teach them those terms explicitly; just explain that if they resist the urge to spend all the money that comes their way, then there is a possibility they could earn more money just for their patience.

You are teaching them about earning interest on their money and a key method to build wealth from an early age! As they get a bit older, you can introduce a 4th jar, labelled ‘invest’ and explain the difference between saving and investing – that each has a purpose, and both are needed. You can distinguish between saving money – subject to inflation, but is necessary to cover emergencies and save for short term goals in cash, then investing – their wealth-building tool.

5. Help them choose how they will give with their money.

Remember that their money is split 3 ways – ‘save’, ‘spend’ and ‘give’. Offer them some options as to how they can help others with their money – perhaps donating to a charity or buying a teacher or friend a small gift.

It’s important that they go through the process of purchasing something for someone else and giving them the gift or actually handing the money to the charity representative. The person’s reaction is almost guaranteed to make your child feel on top of the world. Make a big deal of their feelings – write them down or draw them – you want them to remember how good it feels to help others.

6. Create a mini budget with your child.

Preparation for back-to-school is a perfect time to do this – during the summer they are more likely to have the headspace to really learn and internalize the messages. Sit down and sketch out a budget.

Start with an amount – say 500 AED – and list a range of items that need to be bought along with the prices. Do the sums together – do you have enough for each item? Make sure before you do this with your child that the total of all the school items is slightly more than the budgeted amount. Talk about the options available – we could reprioritise the list to see if there is anything we could take out, search around for cheaper alternatives, or increase the allocated amount for the budget.

Be sure to tell them that in real life it may not always be possible to increase the budget though, so it’s best to try to be creative with the allocated budget first, before just adding more to it. I have another post on saving for back-to-school here if you are interested in more tips to enjoy back-to-school spending without blowing the budget.

7. When your child is a little older, open a savings account together.

Now you can take the idea you have cultivated from the jars method and go along and deposit their money in the bank. Open an internet banking account and track the money together.

The goal is that you encourage them to get hooked on watching money grow before they have a chance to get addicted to spending money. You haven’t got long before consumerist advertisements toxic claws grip your children – it happens to everyone.

Depending on where you are in the world, it may be possible to open an investment account for them too and show them the differences between saving and investing. In the UAE, I invest for my children through Interactive Brokers. I just invest in a different ETF for them than for the adults. When they get a little older (perhaps pre-teen), I plan to show them exactly how their money has grown and what happens to it once they make a trade.

8. Coach them about credit.

As children reach their teens, demonstrate how compound interest can either work for you or against you. Educate your child about the risks (and potential rewards if used sensibly) of credit cards, loans and mortgages. Show them interest charged when you take out credit and a real example of how much something would cost if you bought it with a credit card and only paid off the minimum balance.

You can also offer them the alternative – a person who pays their card off in full each month has the potential to earn cashback and points from a credit card but warn them that these only work for you if you pay the card in full every single month.

On the other hand, you can show them that through investing, compound interest can multiply their money over time. But only if handled sensibly and rationally. Give them a few scenarios and ask them to work through what they would do. For example, John has been paid and wants to buy things and go out, but could invest his money – what should he do? You could compromise and say that John splits his money – some goes towards investing and some towards going out and enjoying the now. This way they can learn the balancing act that is managing money and making decisions about money.

9. Demonstrate gratitude and respect for what you already have.

Perhaps the best money lesson you can pass down is to try to curb the natural human desire for ‘more, more, more’ at an early age. Practise gratitude regularly and openly around your child.

Make it a habit to say every day and out loud how grateful you are for healthy food, a safe house to live in, central heating or air conditioning and a warm bath. These are likely things that your child will take for granted if you have all these staple necessities. Warn them explicitly about the dangers of consumerism, social media and comparison with ‘the Joneses’.

Show them through your own words and actions how much more contented and peaceful it is to live in gratitude for what you have.

10. Share your money story with them.

The final and most important idea is to be honest and open with them. As money is seen as a ‘taboo’ subject, many people grow up in homes whereby money is either not discussed or referred to in a negative way (e.g., ‘we can’t afford it’ or ‘money is the root of all evil’), and they carry this ignorance into their adult lives. The negative cycles are perpetuated.

You can break those cycles by simply being honest and open. Discuss the family finances with your children – your goals and budget. For example, if they really want to impulsively buy something when out shopping, such as a toy, but it isn’t in the budget, explain that if you buy small frivolous items now, perhaps you won’t be able to save for the trip to Disney that you have set as a goal (or whatever it might be).

Show them that you aren’t perfect and tell them your money mistakes. They will relate to you more if you come across as a normal person who makes mistakes than someone who constantly tries to lecture them. Trust me – it will increase their trust in you, not decrease it.

By educating your child in a practical way about money, you can set them up for a successful adult life in so many ways. No matter how we spin it, money underpins everything. Yes, it’s true that money can’t buy happiness, but lack of it or a money struggle can cause real stress and unhappiness.

Being financially literate enables your child to make informed choices. Perhaps they won’t have to be trapped in a toxic work environment or an abusive relationship in the future because you took the time now to show them how to manage their money effectively!

What further tips do you have for teaching children about money? Comment below – I love hearing from you.

Need A Bit Of Support with your finances?

If you would like to book a confidential financial accountability coaching session to help you work on your finances or stay accountable to your goals, send me an email at leapsavvysavers@gmail.com or drop me a line via the contact form and we can see if we’re a good match.

Good luck on your financial journey – congratulations on taking the leap. [...]

Read more...

12 December, 2021Apply / Learn / Save Money / Saving and BudgetingThe year was 2020, and as the world shut its doors on social gatherings, work came flooding in through my email, phone, and devices. In my multi-profession of teacher, tutor and proofreader, demand rose exponentially. As courses went online, people found it more difficult to access work requirements and turned to me to support them. Parents, desperate for children not to fall behind in the wake of a global pandemic, emailed and called for extra sessions. My income increased dramatically.

But here’s the catch. So did my expenses: hello, lifestyle inflation. In amongst all those long working hours and graft, I was dealing with my own anxieties and stresses, which led to throwing my grocery budget out the window entirely. My AC bill went up as we all worked and studied from home, and Amazon became my buddy, joining me in my quest to escape reality: how to function in a world, quaking in the shadow of a deadly virus, uncertain of when life would be ‘normal’ again, and if it ever would.

Don’t get me wrong, I was just about breaking even – due only to the fact that a lot of my expenses had been forcibly reduced – petrol, kid’s activities, travel, and family outings to name a few. However, my spending was spiraling and I wasn’t saving the kind of money I wanted to each month.

What would possess you to refrain from spending for a whole year?

As December 2020 and the new year approached, I decided to get a handle on things. Off work for the school holidays but not travelling anywhere, I knuckled down – I discovered minimalism and decluttered my house, selling a bunch of stuff I didn’t need, and took a long, hard look at my 2020 expenses. I was embarrassed of my grocery bill alone – some months it crept up past 7000aed! I realised I hadn’t taken a deep dive into cutting expenses since I discovered the FIRE (financial independence, retire early) movement in early 2019 as I’d been putting so many hours towards increasing my income by doing side hustles, so it was probably time I reassessed spending.

It was whilst browsing the internet researching cost-cutting ideas one evening when the kids had gone to bed that I came across a couple of ‘no spend year’ Facebook groups. I immediately joined and read through the posts and information. A challenge whereby people didn’t spend money for a whole year except on essentials. It’s so easy to write it off as completely unattainable and undesirable, but I was intrigued. These groups had 10s of thousands of members – this couldn’t be totally out of the realm of possibility. Frugality and minimalism had always interested me, but they were paths I was playing on, dipping my toe in to the waters to test if these concepts were aligned with my values.

Many people will be asking at this point, but why cut expenses? Why make yourself miserable when you could increase your income, making it possible to save, invest, and spend in the present, thus having the best of both worlds? This is great in theory, but myself and my husband are currently low-income earners (I am a teacher, and he is an equestrian instructor) with decade-long freezes on salaries, working part time side hustles to embellish our modest incomes.

Getting a promotion, starting a business, or applying for a better-paying job are all great and I 100% support those goals, but it might not happen overnight, and passive income streams (income that you don’t ‘actively’ earn, such as profit from sales, dividends, or rental income from property) take time and sometimes capital to establish and develop to the point of being passive. Sometimes it’s not as straightforward as just ‘earning more money’ in everyone’s situation.

Also, when people do earn more, they often succumb to lifestyle inflation, as I did in 2020, so being aware of expenses is important for every income level, in my opinion. Plus, with this strategy, you have full control and can implement it immediately. And there’s nothing stopping you from cutting expenses and raising income – it’s not an ‘either, or’ equation. I execute on both strategies simultaneously to maximise my savings rate.

Nevertheless, I had other reasons for wanting to endure this challenge. When people take on a marathon or an iron man challenge, they do so to test themselves, to put themselves through some level of suffering and discomfort purposefully. I wanted the same thing. I’d been following The Minimalists and listening to their podcast for some time and was interested in the idea that in our society, rampant consumerism causes misery rather than happiness and actually prevents us from being our true selves.

If we constantly try to keep up with other people’s or society’s expectations, we become the hamster on the wheel and end up dissatisfied and unfulfilled. One way to shed some of these expectations is by completing a no spend challenge. The burden to spend money to keep up with others will be lifted, albeit in an uncomfortable way, and your creativity and gratitude will be activated. Who knows, you might end up enjoying it?

I realised I wanted to do something big in 2021; I wanted a dramatic change. The series of small changes I’d been implementing had laid a foundation, but I wasn’t achieving the results I wanted. I had spent so long feeling trapped in the ‘rat race’ – not enough savings to move home or work part-time, but a frozen salary and rising living costs in the UAE meant that it was becoming more and more of a struggle to save each month. I felt a burning desire to rise up against my ‘entrapment’ and get on top of it – money, wealth and investments all create options, choices, and autonomy. But it might take short term sacrifice to get them. My grit and resolve kicked in. I felt ready.

For you, it might be a desire to finally shift your debt once and for all, or save 25% for a house deposit, or put your children through university. Whatever it is, it requires much more money in the bank than you currently have. So, you have two options: wish and dream or take massive action. And I’m not talking about robbing a bank or investing in the latest meme stock; both of which are ways to fast track yourself to being broke (and possibly in prison with the first option…). Or you could always take your 1 in 8 million chances of winning the lottery. Personally, I’d prefer a strategy that I have more control over and one that is going to put me out in front – give me an edge.

So, did it work?

Before I get into the planning, preparation and the ‘no spend year’ itself, I want to skip to the present. Sunday 12th December 2021 to be precise. For the purposes of cohesion, my reflection on lessons learned (the softer stuff and the hard, emotional stuff) will come later, so this section is dedicated to the primary reason one endures a no spend challenge: money. Here is a summary of what I achieved during my no spend year:

My core stock market investment portfolio doubled and rose above $100k

I bought a UK rental property, putting a 25% deposit down

I invested in cryptocurrency for the first time

I received a promotion to middle management at work

I started this blog and my LEAP business, which has just started generating sales

More than doubled my net worth (that’s over 100% growth!)

I’d say it worked. A resounding success. It was 100% worth it, not only for the financial rewards that delayed gratification, patience, consistent work, and sacrifice give you, but for all that I learned and all that I became (scroll down for the vulnerable reveal). Ready to dive in? Here comes the practical part – how to plan, prepare and execute your no spend challenge.

Planning and preparation

Ok, once I’d decided to do it – take the proverbial plunge and embark on a ‘no spend year’ – I wondered how on earth one goes about only spending on essentials. A million questions came to mind: what about my kids and husband? Does Netflix count? Can I buy gifts for people? What if my car breaks down? Since it can be confusing, I created a totally free guide and workbook with monthly trackers and FAQs, available here. I will summarise what helped me to prepare for the challenge as well as some tips here:

The first step is to journal/think about/discuss why you want to do this – what piques your interest? What do you want to get out of it? What are you willing and able to put into it? I suggest journaling with pen and paper and allowing yourself freedom to write whatever thoughts enter your head. It may also help to create a vision board and select images, words and quotes that you are drawn to. Another useful technique is to brainstorm on a whiteboard all the reasons for participating in this challenge. This part of the process will help you achieve clarity on your goals, purpose and vision.

The next step is to lay out your rules. You must decide what constitutes a ‘spend day’ and a ‘no spend day’. It’s YOUR challenge and you set the rules. Some people insist that ‘no spend’ is essentials only and nothing else, but I recommend that everyone’s rules be personalised to their circumstances. The idea is that the challenge is tough and gets you out of your comfort zone, but you have to design a program that you can actually stick to long term. Better to do it moderately and endure for a year than go extreme for a month, I say. I would have been more extreme if I didn’t have children, for example. I didn’t want them to be adversely affected by this, so I continued paying for activities that I thought would be beneficial for their development, such as swimming and ballet lessons. I also kept our travel sinking fund, and we visited my husband’s family in Tunisia over the summer. He would have been devastated if I demanded that the trip was cancelled due to my ‘no spend’ challenge. However, I cancelled Netflix, stopped hair and beauty appointments, didn’t buy clothes (and only replaced when they were damaged beyond repair) etc. You have a set of circumstances personal to you, and what’s important is that you consider all the things that you generally spend money on over the course of a year and evaluate each one, then ask – is it going to be in the ‘no spend’ or ‘spend’ category? You could also decide to do it for 20 days of the month or one week – whatever works for you is still progress.

Discuss your intentions with family and friends. It’s going to be difficult to keep it quiet, and it gives you the perfect opportunity to announce that you aren’t going to be ‘conforming’ anymore in a non-defensive way. I would advise you not to try to persuade them to join you though – people don’t tend to take too kindly to that. I looked at the way my family exchanged birthday and Christmas gifts and realised that it was more due to some obligatory expectation than genuine desire to give the gift. So, I explained that I was embarking on a no spend year and that I didn’t want to exchange gifts that lacked meaning. Instead, I offered that we save the money and use it to spend time together (which we would have done anyway) by going on a family outing or indulging in a meal out. They all agreed, but it’s up to you how you approach your friends and family and explain. Most people will be understanding, especially if you offer a compromise.

Track your progress. Once everyone knows and you’ve established your rules, you can get started! Download my free workbook with monthly trackers and keep it simple – one colour for a ‘no spend’ day and a different colour for a ‘spend’ day. Display the monthly tracker somewhere prominent and simply colour in each day depending on how you spent. This allows you to visually track your progress, and forces you to check on, track and be mindful of your spending. To hold yourself super accountable, post your progress on social media (follow my Instagram account @leapsavvysavers for regular updates on my journey) as there is little more motivating than public accountability. All positive outcomes in my book.

Reflect with gratitude, iterate and meet obstacles with action. Reflection is extremely important in this challenge, as is gratitude for everything you have and finding your ‘enough’. Each month (or week or day if it suits you better), reflect upon and journal how you felt, when you felt triggered to spend, and what you achieved. Don’t forget to celebrate your progress and achievements – don’t wait until the end of the year to do this! If it’s too challenging and you feel like giving up, scale it back next month. If you had a disaster and put a load of new clothes on your credit card, don’t give up. Setbacks are normal and part of the process. The best thing to do is figure out what triggered the setback and try to create a pause between the trigger and the action or remove the trigger. For example, have a set of questions in your wallet that you must ask yourself if you want to spend, such as: do I value this item more that the having the money that I am about to exchange for it? How many hours did I have to work to spend this money? Is this something that I will still value in a year? Do I really need this? If internet shopping is the problem, remove your card and login details from the site – you wouldn’t believe how much of a ‘pause’ you can salvage in the time it takes to get up and grab your credit card.

Setbacks and emotions, learning and lessons

It was a bit of an adventure to start – the challenge of the no spend year manifested in some excitement and adrenaline as I got started. Sometimes change, especially when we choose it and design it, feels good. I went about ruthlessly cutting as much as possible from the expenses side of my budget: hair appointments, beauty treatments, clothes – heck, even Netflix was cut. I reasoned that I was spending too much time binge-watching pointless shows on Netflix anyway. That ended up being a good decision as I used the time I had previously been spending watching TV either working on my side hustles or building Leap Savvy Savers. A change from spending time to investing time resulted in much more purpose and fulfillment, the beginnings of a business which I’m proud of, and definitely more money in the bank. I developed a system to cut my grocery bill in half, which you can read in detail here.

My son’s birthday is early February and I got savvy. I decided in early January to have a big declutter and sell as much as I could. The money from the sales equaled the money I spent on his birthday celebrations, essentially making it a zero-sum equation. No need to budget for it. He still got presents, a day out and a cake, but I didn’t use money from the budget to fund it. I got creative with entertaining my kids and invited people to play dates at our house, which usually resulted in an invite back, thus reducing costs on days out. I utilised my husband’s work benefit of free use of a swimming pool to enjoy hours relaxing and swimming with my family without spending money. Packing my own snacks and drinks made it the ultimate frugal day out.

However, it wasn’t all fun, free and frugal days out whilst piles of cash stacked up in my bank account. This is a word of warning about why I believe in a moderate, personalised approach. As the year went on, I found it increasingly more difficult to spend money. My frugality was becoming extreme. There was a turning point. Around June, my husband asked me why I was wearing clothes with holes. My leggings and jeans were so worn out that the seams had started coming apart, and they were really beyond repair. I would always try to cover it with dresses and longer tops, because something was blocking me from replacing the items. He gently encouraged me to replace the clothes.

So, I begrudgingly went to the mall and selected some items (the bare minimum), taking them to the cashier. Standing in the queue, I noticed my anxiety increasing. Palms sweaty, heartrate speeding up. I felt tears stabbing at my eyeballs and my constricting throat threatening a panic attack. In the moment, I didn’t really acknowledge what was happening. I only knew that I didn’t want to part with the money. At all. I didn’t want to spend anything. Was I a failure? Wasn’t I supposedly on a no spend challenge? Suddenly, it was my turn and the cashier smiled and said “yes, ma’am,” beckoning me forward. My brain screamed at me to get out, and I put the clothes down and practically bolted out of the shop. I could barely contain my tears as I raced towards my car and jumped in, slamming the door, and crying hysterically. Why couldn’t I spend money? What was wrong with me?

I realised that I had taken the challenge too far and was experiencing extreme frugality. Not meeting my basic needs just to save money. I was so desperately chasing my goals that I had forgotten how to fulfil my basic needs as a human. I then had to do the hard work of understanding my money blocks and why, instead of finding my ‘enough’, which was my reason for embarking on the challenge, I was being driven by my ‘not enough’. I felt that I wasn’t ‘good enough’, or ‘worthy enough’ unless I took the challenge to the extreme and achieved a certain number in my bank account. I was getting the exact opposite result to what I wanted. It took time and I’m still working on my ability to spend money without guilt and be OK with whatever point I’m at on the journey, but needless to say; I moved a lot of my expense categories over to the ‘no spend’ day rules, turned my validation inward rather than pinning my happiness and fulfillment on achieving some arbitrary goal, and built spending into the budget.

Finding your ‘level’ of no spend is essential to making this work for you. Frugality is good for the soul, the environment and your wallet, but not at the expense of yourself. This challenge is one of the best things I ever did and has changed my way of life. I had some major obstacles and setbacks, most of which I haven’t detailed here, but I developed resilience, discipline and most importantly, self-awareness. Know thyself is the first rule of having a fulfilling and purposeful life, and boy, will this challenge teach you about yourself.

You will face challenges: it might be extreme frugality like me, it might be overspending, or a combination of both – being really ‘good’ all month then blowing everything on the last day. It’s important, essential even, to go through these challenges and try to step outside of the emotions and find the deeper reasons and triggers (therapy is great for this and should be included as an essential expense). If in doubt, lean into deep gratitude for all that you already have and realise that you are enough, whatever the balance in your bank account or however extremely or moderately you approach the no spend year.

Good luck, friend. Connect with me for support, motivation and laughs along the way.

Need a bit of support on your financial journey?

If you would like to book a financial accountability coaching session to help you work through these steps or stay accountable to your goals, send me an email at leapsavvysavers@gmail.com or drop me a line via the contact form and we can see if we are a good match.

Good luck on your financial journey – congratulations on taking the leap. [...]

Read more...

25 September, 2022Apply / Expat Money / Financial Independence / Invest / LearnOne of the most frequently asked questions of expats is ‘what’s the best way to transfer money internationally?’ Expats earning in different currencies than their home currency may have to send money home to support family or meet financial obligations in their home country. In addition, people earning in currencies such as the UAE Dirham (AED) and wanting to fund investments in brokerages that don’t accept AED often want to know the best way to exchange money.

The first thing to consider is what constitutes ‘best’ for you. For some, it’s the lowest cost money transfer, for others convenience is top of their list and for different people safety and reliability of the exchange house. Or it may be a combination of these factors. Quite often, as with most things in life, the cheapest methods are not the most efficient or reliable.

how do i find the best exchange rate?

There are some general costs to consider no matter which method of currency exchange you choose. Keep them in mind as you do your research and ensure before you decide on your exchange method, you have factored in all of the potential costs end to end.

1. International Transfer Fees

You may be charged a fixed fee for exchange, or a percentage of the amount transferred. Either way, some sort of charge is likely to be levied for the exchange by the bank or financial institution doing the currency conversion.

2. Exchange Rate

This one often tricks people. If you see an extremely low (or even free) fee for exchange, check out the exchange rate. Exchange rates vary depending on the supply and demand in the market. Some currencies are ‘pegged’ or fixed, for example the UAE Dirham is pegged to the USA dollar, meaning that they move together.

A ‘spot rate’ or ‘mid-market rate’ is the current asset value, or truest exchange rate possible. However, most banks or financial institutions add a spread to this true rate to increase the charges to you. That way, they can decrease their ‘fees’ but still make money from the exchange; it just won’t be as obvious.

For example, every $1 USD is worth 3.67AED. If every $1 cost you 3.8AED, you could buy less dollars with your dirhams. To simplify this for the purposes of this example:

If you were to buy $10,000 at 3.67AED, you would part with 36,700AED. If you were to exchange at 3.8AED, you would pay 38,000AED. This fractional increase in the spread has just cost you 1300AED. So, when people talk about getting the best possible exchange rate, this is what they mean. The closer it is to the ‘mid-market rate’, the better deal you are getting.

3. Intermediary bank fees

When doing an international transfer, an intermediary bank is often needed. To transfer money, banks must have an account with each other. If the bank you are transferring to doesn’t have an established relationship with your bank, an intermediary will be used and will charge a fee. This is usually around $15-30.

4. Recipient bank Charges

If you transfer to another person via a wire transfer, the bank will often ask you who will bear the fees – the sender or the recipient. This is because the destination bank charges a fee to receive the funds. it’s *usually* cheaper to accept all charges from the sender and you will be able to see how much the total cost will be before you go ahead with the transfer.

Most Efficient way to Transfer Money internationally

It’s best to work out all these potential costs on each method of transfer, then weigh up the best option for you. For example, some financial institutions may give you a better exchange rate but charge a higher fee. You can then decide which is the best overall for your circumstances.

Many expats begin investing into some sort of retirement funds when they move to the Middle East. Often the brokerages do not support their earned currency. You may feel confused or overwhelmed by the thought of investing due to the process of transferring and exchanging money. We often hear ‘keep fees below 1%’ but if you are subject to bank wire transfer fees, you may be paying 4% or more just on transfer, and that’s before you have factored in any sort of charges or commission for actually purchasing your stocks or bonds. So, should we just save in cash while we live overseas and not bother investing? Absolutely not!

There are ways to keep your costs down – some more efficient than others. Here are some common methods that expats use to exchange money. A disclaimer and word of warning though: the fees and terms and conditions of each of these methods is continuously changing and being updated. Therefore, I recommend you do your own research as while I aim to keep my blog up to date, I don’t update every change as soon as they happen. If you get to reading this and the terms and conditions or fees have changed, let me know and I will update the information. Otherwise, take this as a general guide or starting point for your own research.

Secondly, I have not personally used all of the methods discussed below. Some of the information is from my own experience, but much of it is from my research, talking to clients and reaching out to the companies listed. Therefore, if you have a contradictory experience of fees or service etc., please do share below to help the community have a well-rounded and up to date knowledge base to draw from.

1. Bank transfer

This is likely to be the most efficient and reliable as well as most expensive method of transfer. Most banks support international transfers through their internet banking systems – you just have to fill out a form and your money will land in your brokerage the next working day. There aren’t normally any issues as the brokerage can see that the money is coming from your personal bank account in your name.

Due to anti money laundering policies, brokerages often must see that the money is being transferred in your name, otherwise they will return it to you. This is due to financial institutions’ requirement to see the origin of funds. However, you tend to pay for this efficiency and convenience with higher fees and a poor exchange rate. This method can be useful for your first transfer to ‘test the waters’ and try out investing. It’s more important that you get started – you can always optimise as you gain more experience.

2. Revolut

I have heard mixed reviews of Revolut and haven’t personally used them myself, although it is on my to-do list to create an account and give it a go. Some people struggle with opening an account and it is not available to everyone. For UK citizens, if you have a UK address and phone number (which I believe can be changed after the initial setup) you can set up a Revolut UK account. For citizens of the European Economic Area plus Australia, Canada, Singapore, Switzerland, and the United States, you can also open an account in their Lithuania faction.

Once you have an account opened, you can transfer from a limited number of banks in the UAE, including HSBC, ENBD or ADCB (in the branch). If you don’t have an account with one of these banks, you can open a savings account for the purposes of Revolut transfers. Then transfer AED to AED and exchange in Revolut before sending on to Interactive Brokers (or your broker of choice) in your desired currency. Sometimes you may be charged approximately 30AED to transfer out of your UAE bank and Interactive Brokers may hold the money for a few days before you can trade.

Ensure you notify Interactive Brokers that you will be sending money from Revolut by clicking ‘Manage your Account’ then ‘Transfer Funds’ before clicking on ‘Bank Wire’. You also need to specify that you are transferring to another person in Revolut to avoid any money laundering issues.

To transfer from Revolut to Interactive Brokers or another account, you can transfer £1000 for free and after that you will be charged 0.5% unless you pay for a Premium account. At the time of writing, the cost of a Premium account is £6.99 a month or £72 a year. If you wish to make regular payments, it may be worth paying this membership cost to avoid the exchange fees.

3. Wise (formerly Transferwise) and CurrencyFair

Wise, despite previously being a popular option, has become more expensive since they took away the wire transfer for UAE residents and now only give the option of using a debit or credit card, which is more expensive. Therefore, this may not be a viable option anymore.

CurrencyFair on the other hand does have competitive rates. They charge a 0.45% markup on mid-market rates for FOREX and a flat fee of just €3 (or currency equivalent). However, as CurrencyFair is based in Ireland, some people have had issues transferring money from the UAE and, despite it being an AED-to-AED transfer, found themselves with an international transfer fee. It also can be a lengthy process and takes up to 10 days to complete. On the whole, this is a low-cost transfer option, but again not available to all nationalities (the full list is here).

4. Wall Street Exchange and Lulu Exchange

Both of these exchange houses have identical costs, but with Lulu Exchange, you don’t have to visit a branch every time you complete a transfer as you do with Wall Street Exchange. These two have great FX rates, particularly for exchanging to USD. For fluctuating currencies, the spread can range from 0.1%-1%. If you wish to exchange AED for USD, Lulu and Wall Street offer 3.6735 and a fixed fee of 157.5AED.

The service is fast, efficient and reliable too – usually the money lands in its destination within 24 hours. There are no intermediary charges or other hidden fees and only one transaction required by you – transfer the money locally to Lulu or Wall Street and they will remit to Interactive Brokers (or wherever you like) on your behalf.

5. Interactive Brokers

Once your money is in Interactive Brokers, you will get the best rate of currency conversion for no charge and can transfer out for free. However, you do still have to get money into Interactive Brokers using one of the above methods as they don’t accept dirhams (click here for a full list of currencies that Interactive Brokers deals with).

The best exchange rate

There is no perfect or ideal way to make international transfers for every single person. The market is ever-changing and competitive and what works for one person might not work for you. Some people want the lowest cost option and are willing to put in multiple steps manually to avoid fees. Others want convenience and efficiency.

Personally, I find Lulu Exchange suits me the best. I send my contact at Lulu Exchange a WhatsApp message when I am ready to transfer. He acknowledges my message and sends me a receipt. I set up my bank wire notification on Interactive Brokers then transfer the money to Lulu Exchange – FAB to FAB. They then remit the money to Interactive Brokers in the next 24 hours and the receipt breaks down the exact charges and exchange rate.

I like the fact that it is reasonably priced and convenient. I also wait until I have at least $6000 to transfer so that the fees represent a lower percentage of my transfer. If you would like the name and number of my contact in Lulu Exchange, get in touch and I will share the information with you

Options for international money transfer

It is also worth noting that the methods I have outlined are not exhaustive – there are many exchange houses, banks and methods available in the UAE and Middle East. I would recommend that you use a reputable financial institution, regulated by the Central Bank.

Exchange houses can find themselves caught up in controversy and money laundering scams and can be shut down rather swiftly. Smaller, unregulated institutions are much more likely to find themselves in this situation, but larger exchange houses can fall victim too. A few years ago, a large exchange house halted business abruptly and if you happened to be midway through a transfer, it took a long time for funds to be returned. If in doubt, visit the SimplyFI Facebook group for a wealth of information and experience on this topic.

Finally, remember that your money is better in the market so don’t let the process of transferring it hold you up. Try different methods until you find the one that suits you. For the methods listed above, they all have customer services that you can contact and if something goes wrong along the way, your money will be returned to you. Alternatively, you can invest with a robo-advisor such as Stashaway to avoid the international exchange fees. You may still have to transfer money for other reasons, but possibly not as often as if you use an international brokerage to purchase your investments.

What’s your experience with international money transfer? Comment below with your preferred method and why.

[...]

Read more...

11 June, 2021Apply / LearnWhen I first looked at our household spending to analyse areas in which we could cut back and save money, I realised that we were haemorrhaging money on food. It’s easy to do – psychologically, we tell ourselves that this is ‘necessary’ spending. We made every mistake in the book: going shopping with no list, shopping multiple times a week, eating out too often, ordering takeaway because we were too tired to cook after a long day’s work, to name but a few. I figured out quickly that this was the line item that was going to save us the most money, and fast. So, here are 10 steps I developed and still use today to keep grocery spending under control.

1. Plan all your meals and cooking

I started by meal-planning for the following week. Select a day and time and schedule it every week. This will get you in a routine and help you to create a habit. Plan out every meal for the following week for the whole family and most importantly when you will cook. To really save money in this category, limit the number of meals to 2-3 per week and alternate with leftovers. This will mean that you won’t have to buy many ingredients, but you will have to eat the same thing a few times in a row. We don’t mind that in our house and I have trained our kids in this method from when they were toddlers, so they don’t know any different.

2. Shop your house

When you start planning your meals for the following week, begin by shopping your house. Do a quick inventory and check whether you have any items nearing the expiration date. If so, build your meals around those items. Are there any items that would go well together in certain recipes? For example, if you have minced beef and spaghetti, it would make sense to make a spaghetti bolognaise next week. At the same time, you can begin writing your shopping list for other items you may want to purchase as you check your house. I used to buy things all the time only to realise I already had the item lurking at the back of a cupboard. I keep a handy list on my fridge of items I tend to purchase every week, for example, milk, bread and eggs. I check whether these products need replenishing as I am performing my inventory and considering what meals to cook the next week.

3. Use toddler recipe books

One of my personal favourite hacks! I used simple toddler recipes when I was weaning my kids, and I still use them now for many of our meals. They tend to use simple ingredients and be healthy, easy-to-make and budget-friendly meals. The only thing is that they can be bland, so I just add herbs and spices to create more depth of flavour. If you don’t have toddler recipe books, google toddler recipes and there are a huge number of recipes to choose from on the internet.

4. Recipe hacks

I almost always double the recipe on anything I am going to cook. This saves money and time. I also tend to choose meals that I can easily cook in bulk and save the leftovers for the following days. For example, I would be much more likely to choose dinners like casserole, bolognaise, soups, lasagne and curries than meals like fajitas or steak and chips. That is because I can make a huge pot and save it, just cooking some rice, pasta or potatoes the next time I want to feed it to my family. The other recipe hack to try is to cook meals in the same week which use similar ingredients. For example, if I am cooking pesto pasta and I have to buy a jar of pesto but won’t use it all in one dinner, I will search for other recipes using pesto and cook them in the same week.

5. Shop the deals at different places

OK, so you have your meals planned out, have completed your inventory and have created a shopping list. I also include cleaning products and toiletries within the grocery budget, so they will go on the list if they need replacing. At this stage, it may be worth doing a quick check of deals at different supermarkets, although I wouldn’t spend too much time obsessing over this. If you’re not careful, you could spend hours analysing every deal to save just a few dirhams. The time spent researching and buying from different places may not be worth the money saved. You have to calculate that trade-off for yourself, but personally, I tend to spend a few minutes checking whether the big supermarkets have any significant sales or discounts.

Some people also prefer purchasing specific items at certain places; for example, in the UAE, many people like buying their meat and produce from Kibsons as they are reputed to have a superior quality range of these items. However, in general I find that you can save money and time in the long run by buying most of your items at one store. I am all for simplicity and not having to calculate how much one total is and add it to another etcetera. Keeping it straightforward means you are more likely to make this a habit. If you make it too complicated, you are less likely to stick to it week in, week out.

6. Online shopping

This one was a game changer for me. When I switched to online shopping, I saved so much money. I was wary at first, especially about purchasing things like fruit and vegetables, but here in the UAE at least, I have been pleasantly surprised at the quality of items delivered to me. I love that I can shop in my pjs in peace at home when the kids have gone to bed so I can actually focus on what I’m doing. I can easily price compare without having to match the labels on the shelves to the correct items, akin to completing a Rubik’s cube.

I set myself a hard limit for the total amount I will spend on groceries. I ensure that I stick to it by adding whatever is on my list to the shopping cart. Then, when I click on the checkout to pay, if the total is over my budgeted amount, I go through and remove products completely or cut the amount I am buying until I reach my maximum budgeted limit for groceries that week. This is not as difficult as it seems. For example, as you add the items to your cart, you may click on 5 packs of wipes as it is easier to purchase in bulk. But when you get to the checkout, you can reduce to 2 packs as that will see you through the next week as you realise the rest was excess, and thus stick to your budget. If you are over your budgeted amount when you get to the checkout, it also forces you to consider what is necessary for the following week and what you are buying just because you want it.

NB if your budget is too stretched each week and you are struggling to purchase even necessary items, you should consider extending your grocery allowance and looking to make cuts elsewhere in your budget.

7. Buy store brands in bulk

There is an argument for buying in bulk and an argument against buying in bulk, essentially represented by frugalists and minimalists. This blog post is not going to go into the argument for or against as both have merits, and we don’t have the scope here to give them both justice. Needless to say, if something you are purchasing in any case and will use in the future is on sale, then why not purchase in bulk? For example, if you are buying bin bags and you see a great deal for 50% off and you have the capacity to store them in your home, then it may be worth buying them in bulk. Additionally, items such as cleaning products, condiments, frozen fruit and vegetables, medicine, pasta & rice, household staples such as kitchen roll and milk and juice have virtually the same ingredients as their more-expensive branded counterparts. My advice if you are unsure whether to buy store-brand: trial it once. If it lacks quality compared with the branded product, then buy the branded item next time. You might be pleasantly surprised by the quality of home brands and the money you save.

8. Batch cook all your meals and snacks

Right, so you have planned your meals, diligently created your list and completed your online shop. The shopping has been delivered to you. Success! Not quite… A lot of people get so far and fall at this hurdle. Remember in point 1, I said plan out meals and cooking? You should do your meal planning at a certain time of the week, your grocery shopping at a specific time and allocate time to cook. This should be a time when you are not exhausted, busy or overwhelmed. A Wednesday evening at 6pm after a mammoth day of work when you have kids demanding things and the phone is ringing and the doorbell is buzzing is probably not the best time. I opt for a weekend morning – my husband takes the kids out to the park or for a playdate – and I put a Podcast or audiobook on and batch cook for the whole of the next week, or as much as I possibly can.

You have to look at your schedule and see what works for your family, but that works for us at the moment. Is it ideal? No, my ideal scenario would be working part time or freelance so that I can do my batch cooking in the week and free up the entire weekend for my family. But that is not possible right now, so we organise our schedule like this to work towards the ideal scenario. To me, it’s better than dealing with the guilt of throwing away expired food after calling a takeaway because I was too exhausted to cook.

My final hack is that as well as meals, you can batch-cook snacks. I usually cook two large dinners and one or two snacks, such as a batch of blueberry muffins or cereal bars. Saves a ton of money and you have healthy (ish) snacks on hand for hungry kids and lunchboxes. Seriously, do they ever stop eating?

9. Freeze food

This hack helps take the mental load off the primary caregiver who also has to work full-time as well as saving you money. I’ll cook a massive haul of food on a weekend morning, so how do we eat it all before it goes bad? We don’t. I separate it into different Tupperware containers. Whatever we don’t eat that day either goes into the fridge if it is to be eaten over the next couple of days or gets labelled with the name and date and frozen. The result is that you start to build an excess of frozen meals that you can pull out at any given time. If it’s a busy week at work or you aren’t feeling well, you don’t have to reach for a takeaway, you can pull a ready-made meal from the freezer. I use the oldest items first so store them near the front, and fresh food gets stored near the back. This way, you can alternate meals on different days too to alleviate boredom. The same applies to snacks for kids’ lunchboxes – I have built up a stash in the freezer, so I don’t always have to bake at the same rate every week.

10. What if I have to go to the supermarket?

I often visit the supermarket. Perhaps the online delivery service did not stock the item I wanted, or there was a mistake in delivery. I try to do online where possible, but this might happen. Some tips to avoid blowing your budget the minute you step into that golden fortress housing row upon row of shiny objects just waiting to be selected and placed in your trolley:

Lay out your list like the grocery shop that you will most likely shop at. For example, if the toiletries aisle is the first one you walk through when you enter, list toiletries first and so on. This will allow you to work efficiently through the supermarket and stick to your list.

Do not go when you are hungry, stressed or tired. You will buy more.

Look up and down in the aisles. Often, the most expensive items are displayed at eye level.

Schedule your trip right before an appointment so that you have a limited time to finish the shop. This will prevent you from browsing and impulse-spending.

I hope that list of hacks helps you. It seems like a lot, but when you establish a routine, it will all become second nature and I guarantee it will save you money. I managed to slash our grocery budget in half while feeding my family of 4 healthy, wholesome meals. They are simple recipes, but nobody has ever complained in my house! Plus, time has been freed up by scheduling the meal planning, grocery shopping and batch cooking pieces of the ‘feeding a family’ puzzle.

Need a bit of support through these steps?

If you would like to book a financial accountability coaching session to help you work through these steps or stay accountable to your goals, send me an email at leapsavvysavers@gmail.com or drop me a line via the contact form and we can see if we are a good match.

Good luck on your financial journey – congratulations on taking the leap. [...]

Read more...

27 January, 2022Budget / Persist / Saving and BudgetingHow are your new year’s resolutions going? Studies show that up to 80% of people give up their promises to themselves by February. If that’s you, don’t despair! The good news is that you can make a change any time; it just takes a decision, some planning, and sometimes a bit of guidance.

Here is a list of 10 easily actionable goals that you can implement to transform your finances at any time of the year! My biggest tip is start small – just choose one thing to do today and do it. If it’s opening a savings account specifically for your emergency fund or calculating your sinking funds, or ordering one personal finance book, every action makes a difference. Try one of these and let me know how it goes at @leapsavvysavers.

Tip #1 – Calculate your net worth

A snapshot of your financial health, your net worth is a good indicator of your overall financial house health, taken from a bird’s eye view. Tracking it over time can reveal general trends and is a useful evaluation tool when you’re planning financial goals or your budget.

Simply add up all you ‘own’ (cash, property, investments, pensions, some include cars and jewellery as well) and minus all you ‘owe’ (credit card debt, personal loan, mortgage, money owed to people etc.). This number is your net worth. It’s worth tracking it on a semi-regular basis (I do it every quarter, some do it bi-annually or even monthly if it helps you). It’s not the most important or reliable metric as it’s often subject to market fluctuations; however, it does give a snapshot of your financial picture and you can track it over time to assess whether, overall, you’re on an upward trend.

Tip #2 – Create a realistic budget

Even if you don’t have debt or you are a high income-earner, a budget is your friend. Take the time to track your expenses and use this to create categories. Once you’ve tracked backwards, plan forwards and assign each dirham (or dollar or pound depending on where you earn) a duty to spend more intentionally and become the boss of your money. Don’t forget to reconcile at the end of the month – match your actual spending to your budgeted – in order to plan ahead to the next month. For an easy to use annual budget template with all formulas already plugged in, click here.

Tip #3 – Plan for the win

Use your calendar to plot out spending for the year. Plug in birthdays, events, religious celebrations, subscription renewals, annual medical check-ups, insurance renewals, ID and paperwork updates – literally anything that you KNOW will cost you money. Then put it in your budget. Decide whether it is going to be cash flowed (come from your monthly budget) or paid for by a sinking fund (larger predicted expenses over a 12-month period, which you can save for incrementally).

Should you decide you want to pay for it from your sinking funds, add up the total of these items or events, divide by 12 and start saving that amount into a separate savings account. For example, you might decide that you want to spend a relatively small amount for your friend’s birthday gift, so you will work it into your monthly budget and pay for it from your salary. However, you may want your child’s birthday this year to include a party, outing, presents and cake, in which case it will be too large to pay for in one month’s budget, along with your groceries and bills etc. Then it becomes a sinking fund and you spread the cost over several months.

Tip #4 – Build your emergency fund

What about the unexpected? I hear you asking the question as I write about sinking funds. The best laid plans, huh? No matter how meticulously we colour-code our calendars and plan out our perfect zero-based budgets, we just can’t plan for everything. That’s where an emergency fund dons its cape and saves us from crushing credit card debt. Typically, financial advice recommends having 3-6 months’ worth of expenses tucked away in a separate savings account for, well, rainy days – unexpected events such as a sudden job loss or your car breaks down.

I think this number is extremely personal – some people want the comfort of lots of cash on hand while others feel comfortable investing the vast majority of their money and keep a fairly small amount of cash. It really depends on your risk tolerance and personal circumstances – how many people do you have that are dependent on your income for example? Whatever you decide, its best to have some cash buffer available. Download my FREE emergency fund tracker here to save your way to being able to weather any financial storm.

Tip #5 – Knowledge = confidence

Financial confidence is born out of knowledge. You don’t need to know everything about options trading or NFTs, but foundational financial literacy is fundamental to building successful systems and structures, and most importantly, staying the course in the face of a multitude of temptations and latest trends etc. You could make it a goal to read one finance book a month or listen to one podcast episode a week. When you start consuming the literature, you can apply the strategies that suit you and check validity – if multiple authors and podcast presenters agree on a certain concept, it is likely to be an established wealth-building method. I update my book recommendations page regularly with interesting books in the areas of investing, money mindset and personal development.

I also always set aside part of my sinking fund for my education – whether that be a course, a training programme or books – the best investment is in yourself as it is the one that you can guarantee a return on investment IF you take action to implement the tips, strategies and knowledge you learn. With that in mind, if you want a very reasonably priced course that walks you through every aspect of money management, from budgeting, to savings rate, to sinking funds, to emergency funds, then I have just the one! Alternatively, if you feel that an investing course is more your cup of tea, this is a brilliant one – I have taken it and personally recommend.

Tip #6 – Start with the end in mind

Have you ever thought about how and why you set goals? Setting goals is a much-debated topic – some people love them, others hate them. I think they can be useful, IF they are rooted in your values, what you truly want. You have to put the reflective inner work in to figure out what that is, start with a big picture vision, then work backwards and ask yourself: what can I realistically achieve this year to move in the direction of my big picture vision? Personally, I think goals should sit in the just-out-of-reach region, not easily achieved but not completely out of the realm of possibility either.

Break down annual goals into monthly, weekly, and daily goals to muster the consistency needed to achieve a big vision, such as retirement or becoming a millionaire. You can work out your estimated FI (financial independence) number relatively easily using the rule of 25 – multiply your annual expenses by 25 (for example, if you spend approximately $40k a year, you will need $1 million invested to become financially independent). For most people, that figure is huge and can feel overwhelming, but if you break it down and aim for the first $12k, that’s $1k a month and so on.

Tip #7 –Solve your future problems