The year was 2020, and as the world shut its doors on social gatherings, work came flooding in through my email, phone, and devices. In my multi-profession of teacher, tutor and proofreader, demand rose exponentially. As courses went online, people found it more difficult to access work requirements and turned to me to support them. Parents, desperate for children not to fall behind in the wake of a global pandemic, emailed and called for extra sessions. My income increased dramatically.

But here’s the catch. So did my expenses: hello, lifestyle inflation. In amongst all those long working hours and graft, I was dealing with my own anxieties and stresses, which led to throwing my grocery budget out the window entirely. My AC bill went up as we all worked and studied from home, and Amazon became my buddy, joining me in my quest to escape reality: how to function in a world, quaking in the shadow of a deadly virus, uncertain of when life would be ‘normal’ again, and if it ever would.

Don’t get me wrong, I was just about breaking even – due only to the fact that a lot of my expenses had been forcibly reduced – petrol, kid’s activities, travel, and family outings to name a few. However, my spending was spiraling and I wasn’t saving the kind of money I wanted to each month.

What would possess you to refrain from spending for a whole year?

As December 2020 and the new year approached, I decided to get a handle on things. Off work for the school holidays but not travelling anywhere, I knuckled down – I discovered minimalism and decluttered my house, selling a bunch of stuff I didn’t need, and took a long, hard look at my 2020 expenses. I was embarrassed of my grocery bill alone – some months it crept up past 7000aed! I realised I hadn’t taken a deep dive into cutting expenses since I discovered the FIRE (financial independence, retire early) movement in early 2019 as I’d been putting so many hours towards increasing my income by doing side hustles, so it was probably time I reassessed spending.

It was whilst browsing the internet researching cost-cutting ideas one evening when the kids had gone to bed that I came across a couple of ‘no spend year’ Facebook groups. I immediately joined and read through the posts and information. A challenge whereby people didn’t spend money for a whole year except on essentials. It’s so easy to write it off as completely unattainable and undesirable, but I was intrigued. These groups had 10s of thousands of members – this couldn’t be totally out of the realm of possibility. Frugality and minimalism had always interested me, but they were paths I was playing on, dipping my toe in to the waters to test if these concepts were aligned with my values.

Many people will be asking at this point, but why cut expenses? Why make yourself miserable when you could increase your income, making it possible to save, invest, and spend in the present, thus having the best of both worlds? This is great in theory, but myself and my husband are currently low-income earners (I am a teacher, and he is an equestrian instructor) with decade-long freezes on salaries, working part time side hustles to embellish our modest incomes.

Getting a promotion, starting a business, or applying for a better-paying job are all great and I 100% support those goals, but it might not happen overnight, and passive income streams (income that you don’t ‘actively’ earn, such as profit from sales, dividends, or rental income from property) take time and sometimes capital to establish and develop to the point of being passive. Sometimes it’s not as straightforward as just ‘earning more money’ in everyone’s situation.

Also, when people do earn more, they often succumb to lifestyle inflation, as I did in 2020, so being aware of expenses is important for every income level, in my opinion. Plus, with this strategy, you have full control and can implement it immediately. And there’s nothing stopping you from cutting expenses and raising income – it’s not an ‘either, or’ equation. I execute on both strategies simultaneously to maximise my savings rate.

Nevertheless, I had other reasons for wanting to endure this challenge. When people take on a marathon or an iron man challenge, they do so to test themselves, to put themselves through some level of suffering and discomfort purposefully. I wanted the same thing. I’d been following The Minimalists and listening to their podcast for some time and was interested in the idea that in our society, rampant consumerism causes misery rather than happiness and actually prevents us from being our true selves.

If we constantly try to keep up with other people’s or society’s expectations, we become the hamster on the wheel and end up dissatisfied and unfulfilled. One way to shed some of these expectations is by completing a no spend challenge. The burden to spend money to keep up with others will be lifted, albeit in an uncomfortable way, and your creativity and gratitude will be activated. Who knows, you might end up enjoying it?

I realised I wanted to do something big in 2021; I wanted a dramatic change. The series of small changes I’d been implementing had laid a foundation, but I wasn’t achieving the results I wanted. I had spent so long feeling trapped in the ‘rat race’ – not enough savings to move home or work part-time, but a frozen salary and rising living costs in the UAE meant that it was becoming more and more of a struggle to save each month. I felt a burning desire to rise up against my ‘entrapment’ and get on top of it – money, wealth and investments all create options, choices, and autonomy. But it might take short term sacrifice to get them. My grit and resolve kicked in. I felt ready.

For you, it might be a desire to finally shift your debt once and for all, or save 25% for a house deposit, or put your children through university. Whatever it is, it requires much more money in the bank than you currently have. So, you have two options: wish and dream or take massive action. And I’m not talking about robbing a bank or investing in the latest meme stock; both of which are ways to fast track yourself to being broke (and possibly in prison with the first option…). Or you could always take your 1 in 8 million chances of winning the lottery. Personally, I’d prefer a strategy that I have more control over and one that is going to put me out in front – give me an edge.

So, did it work?

Before I get into the planning, preparation and the ‘no spend year’ itself, I want to skip to the present. Sunday 12th December 2021 to be precise. For the purposes of cohesion, my reflection on lessons learned (the softer stuff and the hard, emotional stuff) will come later, so this section is dedicated to the primary reason one endures a no spend challenge: money. Here is a summary of what I achieved during my no spend year:

- My core stock market investment portfolio doubled and rose above $100k

- I bought a UK rental property, putting a 25% deposit down

- I invested in cryptocurrency for the first time

- I received a promotion to middle management at work

- I started this blog and my LEAP business, which has just started generating sales

- More than doubled my net worth (that’s over 100% growth!)

I’d say it worked. A resounding success. It was 100% worth it, not only for the financial rewards that delayed gratification, patience, consistent work, and sacrifice give you, but for all that I learned and all that I became (scroll down for the vulnerable reveal). Ready to dive in? Here comes the practical part – how to plan, prepare and execute your no spend challenge.

Planning and preparation

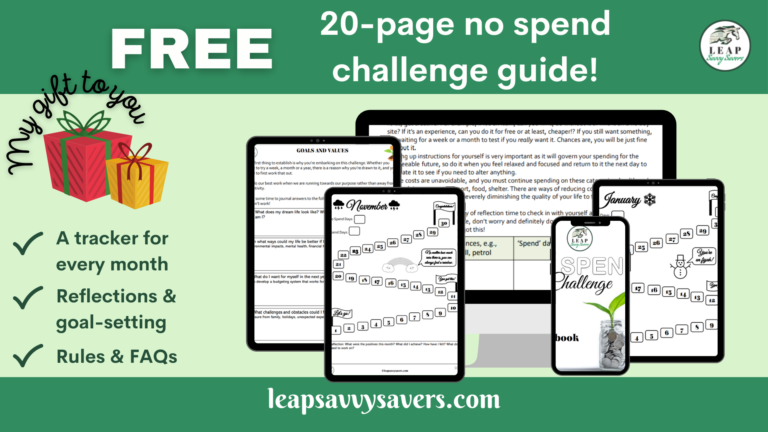

Ok, once I’d decided to do it – take the proverbial plunge and embark on a ‘no spend year’ – I wondered how on earth one goes about only spending on essentials. A million questions came to mind: what about my kids and husband? Does Netflix count? Can I buy gifts for people? What if my car breaks down? Since it can be confusing, I created a totally free guide and workbook with monthly trackers and FAQs, available here. I will summarise what helped me to prepare for the challenge as well as some tips here:

- The first step is to journal/think about/discuss why you want to do this – what piques your interest? What do you want to get out of it? What are you willing and able to put into it? I suggest journaling with pen and paper and allowing yourself freedom to write whatever thoughts enter your head. It may also help to create a vision board and select images, words and quotes that you are drawn to. Another useful technique is to brainstorm on a whiteboard all the reasons for participating in this challenge. This part of the process will help you achieve clarity on your goals, purpose and vision.

- The next step is to lay out your rules. You must decide what constitutes a ‘spend day’ and a ‘no spend day’. It’s YOUR challenge and you set the rules. Some people insist that ‘no spend’ is essentials only and nothing else, but I recommend that everyone’s rules be personalised to their circumstances. The idea is that the challenge is tough and gets you out of your comfort zone, but you have to design a program that you can actually stick to long term. Better to do it moderately and endure for a year than go extreme for a month, I say. I would have been more extreme if I didn’t have children, for example. I didn’t want them to be adversely affected by this, so I continued paying for activities that I thought would be beneficial for their development, such as swimming and ballet lessons. I also kept our travel sinking fund, and we visited my husband’s family in Tunisia over the summer. He would have been devastated if I demanded that the trip was cancelled due to my ‘no spend’ challenge. However, I cancelled Netflix, stopped hair and beauty appointments, didn’t buy clothes (and only replaced when they were damaged beyond repair) etc. You have a set of circumstances personal to you, and what’s important is that you consider all the things that you generally spend money on over the course of a year and evaluate each one, then ask – is it going to be in the ‘no spend’ or ‘spend’ category? You could also decide to do it for 20 days of the month or one week – whatever works for you is still progress.

- Discuss your intentions with family and friends. It’s going to be difficult to keep it quiet, and it gives you the perfect opportunity to announce that you aren’t going to be ‘conforming’ anymore in a non-defensive way. I would advise you not to try to persuade them to join you though – people don’t tend to take too kindly to that. I looked at the way my family exchanged birthday and Christmas gifts and realised that it was more due to some obligatory expectation than genuine desire to give the gift. So, I explained that I was embarking on a no spend year and that I didn’t want to exchange gifts that lacked meaning. Instead, I offered that we save the money and use it to spend time together (which we would have done anyway) by going on a family outing or indulging in a meal out. They all agreed, but it’s up to you how you approach your friends and family and explain. Most people will be understanding, especially if you offer a compromise.

- Track your progress. Once everyone knows and you’ve established your rules, you can get started! Download my free workbook with monthly trackers and keep it simple – one colour for a ‘no spend’ day and a different colour for a ‘spend’ day. Display the monthly tracker somewhere prominent and simply colour in each day depending on how you spent. This allows you to visually track your progress, and forces you to check on, track and be mindful of your spending. To hold yourself super accountable, post your progress on social media (follow my Instagram account @leapsavvysavers for regular updates on my journey) as there is little more motivating than public accountability. All positive outcomes in my book.

- Reflect with gratitude, iterate and meet obstacles with action. Reflection is extremely important in this challenge, as is gratitude for everything you have and finding your ‘enough’. Each month (or week or day if it suits you better), reflect upon and journal how you felt, when you felt triggered to spend, and what you achieved. Don’t forget to celebrate your progress and achievements – don’t wait until the end of the year to do this! If it’s too challenging and you feel like giving up, scale it back next month. If you had a disaster and put a load of new clothes on your credit card, don’t give up. Setbacks are normal and part of the process. The best thing to do is figure out what triggered the setback and try to create a pause between the trigger and the action or remove the trigger. For example, have a set of questions in your wallet that you must ask yourself if you want to spend, such as: do I value this item more that the having the money that I am about to exchange for it? How many hours did I have to work to spend this money? Is this something that I will still value in a year? Do I really need this? If internet shopping is the problem, remove your card and login details from the site – you wouldn’t believe how much of a ‘pause’ you can salvage in the time it takes to get up and grab your credit card.

Setbacks and emotions, learning and lessons

It was a bit of an adventure to start – the challenge of the no spend year manifested in some excitement and adrenaline as I got started. Sometimes change, especially when we choose it and design it, feels good. I went about ruthlessly cutting as much as possible from the expenses side of my budget: hair appointments, beauty treatments, clothes – heck, even Netflix was cut. I reasoned that I was spending too much time binge-watching pointless shows on Netflix anyway. That ended up being a good decision as I used the time I had previously been spending watching TV either working on my side hustles or building Leap Savvy Savers. A change from spending time to investing time resulted in much more purpose and fulfillment, the beginnings of a business which I’m proud of, and definitely more money in the bank. I developed a system to cut my grocery bill in half, which you can read in detail here.

My son’s birthday is early February and I got savvy. I decided in early January to have a big declutter and sell as much as I could. The money from the sales equaled the money I spent on his birthday celebrations, essentially making it a zero-sum equation. No need to budget for it. He still got presents, a day out and a cake, but I didn’t use money from the budget to fund it. I got creative with entertaining my kids and invited people to play dates at our house, which usually resulted in an invite back, thus reducing costs on days out. I utilised my husband’s work benefit of free use of a swimming pool to enjoy hours relaxing and swimming with my family without spending money. Packing my own snacks and drinks made it the ultimate frugal day out.

However, it wasn’t all fun, free and frugal days out whilst piles of cash stacked up in my bank account. This is a word of warning about why I believe in a moderate, personalised approach. As the year went on, I found it increasingly more difficult to spend money. My frugality was becoming extreme. There was a turning point. Around June, my husband asked me why I was wearing clothes with holes. My leggings and jeans were so worn out that the seams had started coming apart, and they were really beyond repair. I would always try to cover it with dresses and longer tops, because something was blocking me from replacing the items. He gently encouraged me to replace the clothes.

So, I begrudgingly went to the mall and selected some items (the bare minimum), taking them to the cashier. Standing in the queue, I noticed my anxiety increasing. Palms sweaty, heartrate speeding up. I felt tears stabbing at my eyeballs and my constricting throat threatening a panic attack. In the moment, I didn’t really acknowledge what was happening. I only knew that I didn’t want to part with the money. At all. I didn’t want to spend anything. Was I a failure? Wasn’t I supposedly on a no spend challenge? Suddenly, it was my turn and the cashier smiled and said “yes, ma’am,” beckoning me forward. My brain screamed at me to get out, and I put the clothes down and practically bolted out of the shop. I could barely contain my tears as I raced towards my car and jumped in, slamming the door, and crying hysterically. Why couldn’t I spend money? What was wrong with me?

I realised that I had taken the challenge too far and was experiencing extreme frugality. Not meeting my basic needs just to save money. I was so desperately chasing my goals that I had forgotten how to fulfil my basic needs as a human. I then had to do the hard work of understanding my money blocks and why, instead of finding my ‘enough’, which was my reason for embarking on the challenge, I was being driven by my ‘not enough’. I felt that I wasn’t ‘good enough’, or ‘worthy enough’ unless I took the challenge to the extreme and achieved a certain number in my bank account. I was getting the exact opposite result to what I wanted. It took time and I’m still working on my ability to spend money without guilt and be OK with whatever point I’m at on the journey, but needless to say; I moved a lot of my expense categories over to the ‘no spend’ day rules, turned my validation inward rather than pinning my happiness and fulfillment on achieving some arbitrary goal, and built spending into the budget.

Finding your ‘level’ of no spend is essential to making this work for you. Frugality is good for the soul, the environment and your wallet, but not at the expense of yourself. This challenge is one of the best things I ever did and has changed my way of life. I had some major obstacles and setbacks, most of which I haven’t detailed here, but I developed resilience, discipline and most importantly, self-awareness. Know thyself is the first rule of having a fulfilling and purposeful life, and boy, will this challenge teach you about yourself.

You will face challenges: it might be extreme frugality like me, it might be overspending, or a combination of both – being really ‘good’ all month then blowing everything on the last day. It’s important, essential even, to go through these challenges and try to step outside of the emotions and find the deeper reasons and triggers (therapy is great for this and should be included as an essential expense). If in doubt, lean into deep gratitude for all that you already have and realise that you are enough, whatever the balance in your bank account or however extremely or moderately you approach the no spend year.

Good luck, friend. Connect with me for support, motivation and laughs along the way.

Need a bit of support on your financial journey?

If you would like to book a financial accountability coaching session to help you work through these steps or stay accountable to your goals, send me an email at leapsavvysavers@gmail.com or drop me a line via the contact form and we can see if we are a good match. Good luck on your financial journey – congratulations on taking the leap.