How are your new year’s resolutions going? Studies show that up to 80% of people give up their promises to themselves by February. If that’s you, don’t despair! The good news is that you can make a change any time; it just takes a decision, some planning, and sometimes a bit of guidance.

Here is a list of 10 easily actionable goals that you can implement to transform your finances at any time of the year! My biggest tip is start small – just choose one thing to do today and do it. If it’s opening a savings account specifically for your emergency fund or calculating your sinking funds, or ordering one personal finance book, every action makes a difference. Try one of these and let me know how it goes at @leapsavvysavers.

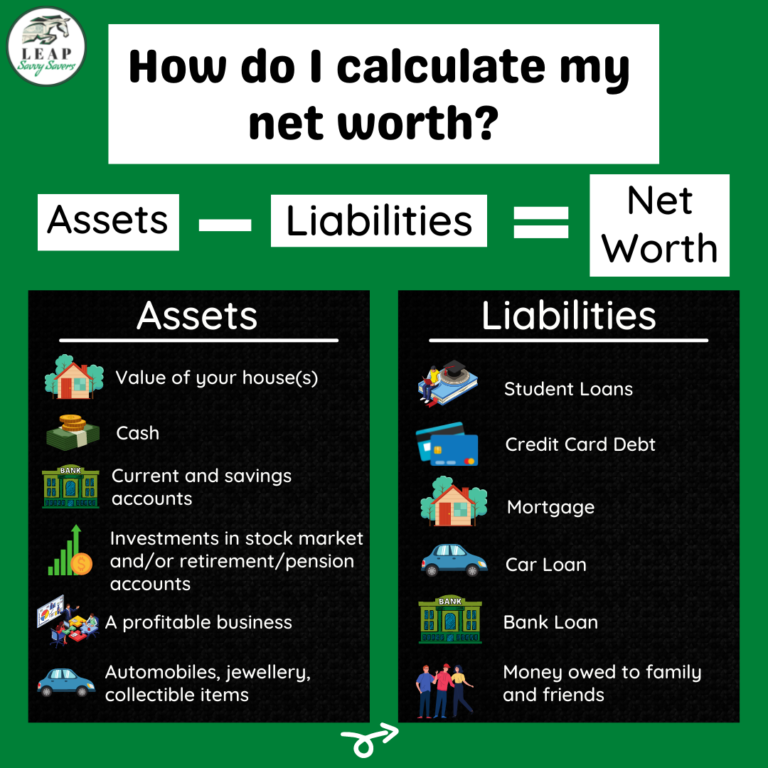

Tip #1 - Calculate your net worth

A snapshot of your financial health, your net worth is a good indicator of your overall financial house health, taken from a bird’s eye view. Tracking it over time can reveal general trends and is a useful evaluation tool when you’re planning financial goals or your budget.

Simply add up all you ‘own’ (cash, property, investments, pensions, some include cars and jewellery as well) and minus all you ‘owe’ (credit card debt, personal loan, mortgage, money owed to people etc.). This number is your net worth. It’s worth tracking it on a semi-regular basis (I do it every quarter, some do it bi-annually or even monthly if it helps you). It’s not the most important or reliable metric as it’s often subject to market fluctuations; however, it does give a snapshot of your financial picture and you can track it over time to assess whether, overall, you’re on an upward trend.

Tip #2 - Create a realistic budget

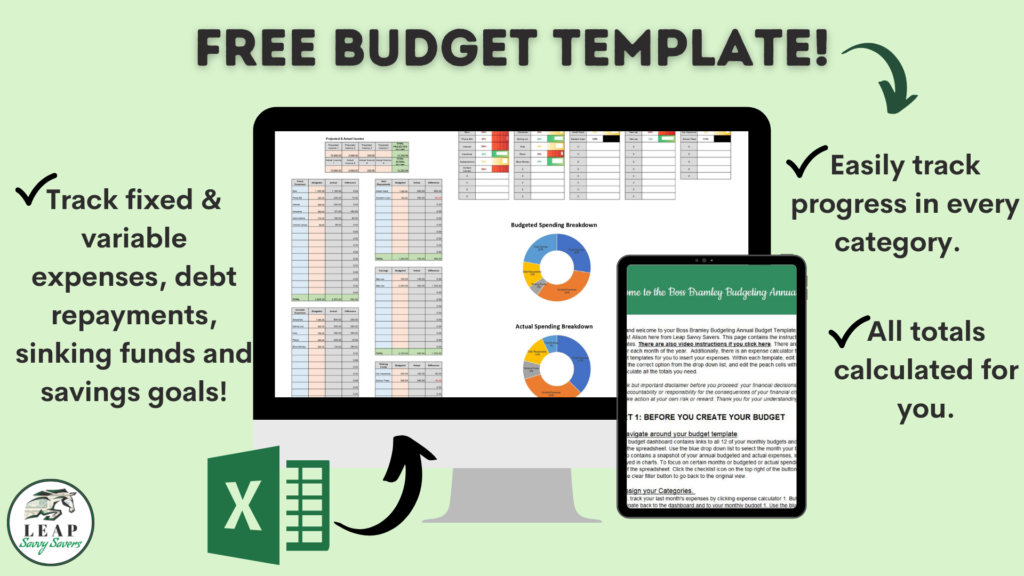

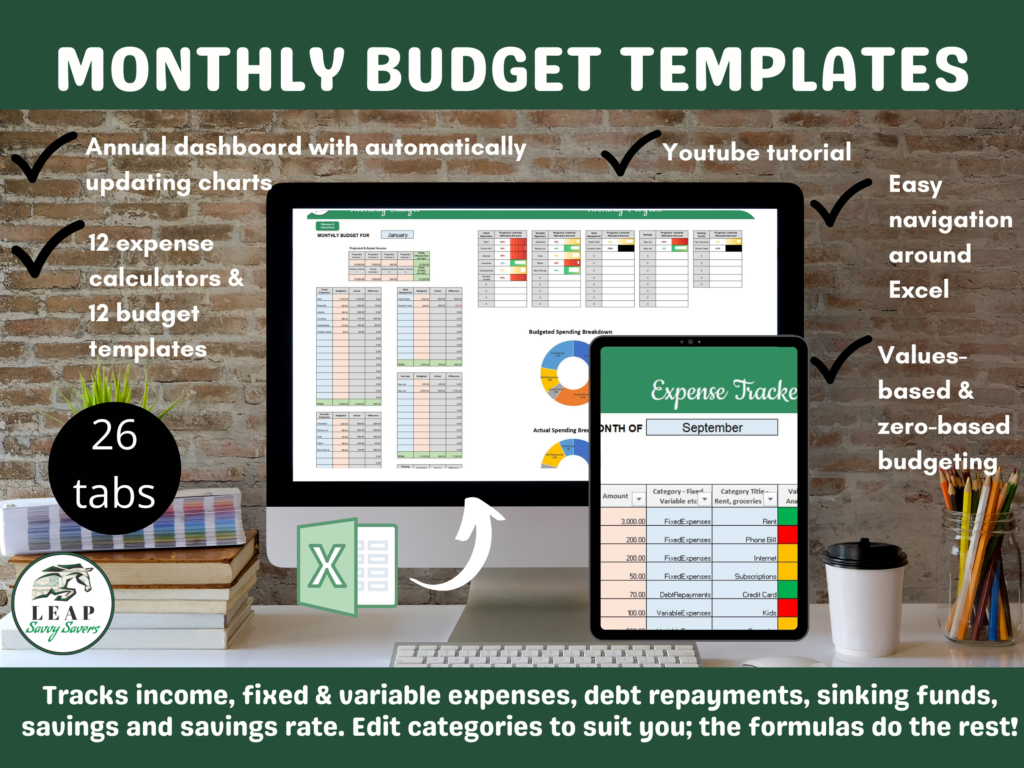

Even if you don’t have debt or you are a high income-earner, a budget is your friend. Take the time to track your expenses and use this to create categories. Once you’ve tracked backwards, plan forwards and assign each dirham (or dollar or pound depending on where you earn) a duty to spend more intentionally and become the boss of your money. Don’t forget to reconcile at the end of the month – match your actual spending to your budgeted – in order to plan ahead to the next month. For an easy to use annual budget template with all formulas already plugged in, click here.

Tip #3 - Plan for the win

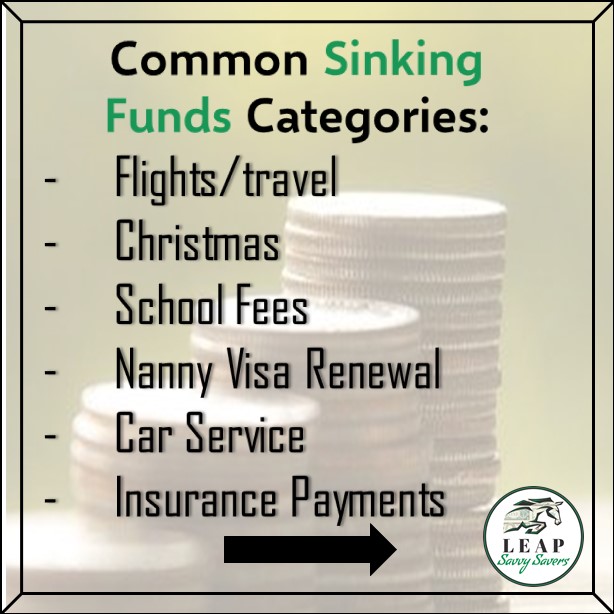

Use your calendar to plot out spending for the year. Plug in birthdays, events, religious celebrations, subscription renewals, annual medical check-ups, insurance renewals, ID and paperwork updates – literally anything that you KNOW will cost you money. Then put it in your budget. Decide whether it is going to be cash flowed (come from your monthly budget) or paid for by a sinking fund (larger predicted expenses over a 12-month period, which you can save for incrementally).

Should you decide you want to pay for it from your sinking funds, add up the total of these items or events, divide by 12 and start saving that amount into a separate savings account. For example, you might decide that you want to spend a relatively small amount for your friend’s birthday gift, so you will work it into your monthly budget and pay for it from your salary. However, you may want your child’s birthday this year to include a party, outing, presents and cake, in which case it will be too large to pay for in one month’s budget, along with your groceries and bills etc. Then it becomes a sinking fund and you spread the cost over several months.

Tip #4 – Build your emergency fund

What about the unexpected? I hear you asking the question as I write about sinking funds. The best laid plans, huh? No matter how meticulously we colour-code our calendars and plan out our perfect zero-based budgets, we just can’t plan for everything. That’s where an emergency fund dons its cape and saves us from crushing credit card debt. Typically, financial advice recommends having 3-6 months’ worth of expenses tucked away in a separate savings account for, well, rainy days – unexpected events such as a sudden job loss or your car breaks down.

I think this number is extremely personal – some people want the comfort of lots of cash on hand while others feel comfortable investing the vast majority of their money and keep a fairly small amount of cash. It really depends on your risk tolerance and personal circumstances – how many people do you have that are dependent on your income for example? Whatever you decide, its best to have some cash buffer available. Download my FREE emergency fund tracker here to save your way to being able to weather any financial storm.

Tip #5 – Knowledge = confidence

Financial confidence is born out of knowledge. You don’t need to know everything about options trading or NFTs, but foundational financial literacy is fundamental to building successful systems and structures, and most importantly, staying the course in the face of a multitude of temptations and latest trends etc. You could make it a goal to read one finance book a month or listen to one podcast episode a week. When you start consuming the literature, you can apply the strategies that suit you and check validity – if multiple authors and podcast presenters agree on a certain concept, it is likely to be an established wealth-building method. I update my book recommendations page regularly with interesting books in the areas of investing, money mindset and personal development.

I also always set aside part of my sinking fund for my education – whether that be a course, a training programme or books – the best investment is in yourself as it is the one that you can guarantee a return on investment IF you take action to implement the tips, strategies and knowledge you learn. With that in mind, if you want a very reasonably priced course that walks you through every aspect of money management, from budgeting, to savings rate, to sinking funds, to emergency funds, then I have just the one! Alternatively, if you feel that an investing course is more your cup of tea, this is a brilliant one – I have taken it and personally recommend.

Tip #6 – Start with the end in mind

Have you ever thought about how and why you set goals? Setting goals is a much-debated topic – some people love them, others hate them. I think they can be useful, IF they are rooted in your values, what you truly want. You have to put the reflective inner work in to figure out what that is, start with a big picture vision, then work backwards and ask yourself: what can I realistically achieve this year to move in the direction of my big picture vision? Personally, I think goals should sit in the just-out-of-reach region, not easily achieved but not completely out of the realm of possibility either.

Break down annual goals into monthly, weekly, and daily goals to muster the consistency needed to achieve a big vision, such as retirement or becoming a millionaire. You can work out your estimated FI (financial independence) number relatively easily using the rule of 25 – multiply your annual expenses by 25 (for example, if you spend approximately $40k a year, you will need $1 million invested to become financially independent). For most people, that figure is huge and can feel overwhelming, but if you break it down and aim for the first $12k, that’s $1k a month and so on.

Tip #7 –Solve your future problems

A great tip I learned last year was to plan for challenges ahead of time. For example, you might set a goal to save $1000 a month and in January when things are quiet, you may easily achieve your goal. But have you considered when temptation strikes, whatever that might be for you? It might be birthdays, Christmas, Eid, payday, online shopping, nights out, when you feel stressed, when you feel happy, when you feel homesick – most of us have spending triggers. Once you identify yours, you’ll be better placed to prepare your actions for when the temptation inevitably bubbles up.

For example, if I feel the impulse to shop on Amazon, I will drink 1 litre of water and do 20-star jumps. Then, if I still want to browse, I will put items in my cart and leave them there for 7 days. If I still want the item, I then give myself permission to purchase. The ‘pause’ created by your new routine will be enough disruption to the habit to give you time to logically review your choices and not give in to the impulse in 9 out of 10 situations. Build these behaviours and routines for each distraction to your goals, and keep your goals visually accessible, for example on your desktop screensaver or stuck on your fridge.

Tip #8 – Increase your income

When you’re looking at your income and expenses and assessing how you can grow your savings rate, you really have two choices: reduce expenses or increase income. For many people, increasing income is the more attractive option. There is a limit to how much you can save, but earning potential is limitless. You have loads of options – start a side hustle, work towards a promotion, spruce up your CV to apply for new jobs, learn a high-income and in-demand skill… Be creative and think outside the box – I think a good place to start is by filling in an Ikigai diagram, considering what you love, what you can be paid for, what the world needs and where your skills lie. Within that brainstorming, you may discover the perfect side hustle – I did with Leap Savvy Savers!

However, many people don’t want to do a side hustle and it’s not for everyone – there are usually longer hours involved as you set it up and it may impact your free time. Therefore, working towards a promotion might be for you – could you schedule a meeting with your line manager to plan a strategy for working towards a promotion or starting a training course? Or could you spruce up your CV and apply for higher paying roles. Honestly, the possibilities are endless and the potential to earn income is limitless, so make it a goal this year to plan a strategy to raise your income.

Tip #9 – Supercharge your savings

You might love your modestly-paying job or have other commitments, or just simply not fancy extra training or longer hours. In that case, you can supercharge your savings instead. You might think that you can’t save anymore and that you already live modestly, but I am here to challenge that limiting belief! You have a few options if you want to cut back on your spending:

- Try a no spend challenge – I did this and it’s not as bad as it first seems – I did it and not only survived but thrived! In a nutshell, you set yourself a challenge to cut back as much non-essential spending as you can, then track your progress. You might set yourself a goal of 20 days or no buying non-essentials for a whole month. There’s nothing stopping you from adding these line items back into your budget, and the bonus: you don’t know what you really, truly value until you go without. Only then will you know what you really want to add back into your monthly spending.

- Start tracking your savings rate. It’s pretty easy – just add up all your income and minus all your expenses. Once you do this, you have a savings rate, then just convert that number into a percentage; for example, if you earn $1000 and spend $500, your savings rate is 1000-500=500/1000=0.5×100 = 50%. Just tracking this number can motivate you to improve it – challenge yourself to improve it by 1-5% next month by taking on a savings challenge.

- Cut your expenses methodically. If you don’t fancy a no-spend challenge, then you could work through your expenses category-by-category. I would start with fixed expenses (expenses that generally don’t change month-to-month such as rent, phone bill or subscriptions) – see if you can call your service providers to negotiate a lower rate or cut some out altogether. Then, move on to variable expenses (any expenses that fluctuate each month, such as clothing or days out). Evaluate each expense for how much value it brought you (you could rate on a scale of 1-10) and that will help you decide which are best to keep and which you can bin! For example, if you love going out to eat every Friday, then keep doing that. On the other hand, if you are paying for clothes and shoes each month that you don’t even get a chance to wear, it might be best to decrease that category in your budget.

Tip #10 – Practise daily gratitude

My final tip is probably the most important! I can’t tell you how long I underestimated gratitude, writing it off as ‘woo, woo’ and not something productive that would help me feel accomplished. That was my old way of thinking. Gratitude and reflection are the key ingredients in figuring out what accomplishment even means for you, instead of simply following society’s/family’s/spouse’s expectations of you. Gratitude helped me save money by taming my desire for more (more achievement, more stuff, more everything) and instead, being content with what already is.

Developing a simple habit of writing 3 things you are grateful for every night before bed can help you save money and replace the feeling of being restricted by your budget with the freedom that comes (or will come if you stay the course!) from being disciplined and living within your means. I try to vary the things I feel grateful for each day – everything from the big things – like being interviewed on the radio with Helen Farmer – to a fresh cup of coffee, or my personal favourite – when my 3 year old daughter tells me how pretty I am! There are a multitude of other ways that practising gratitude will benefit your life that I haven’t mentioned here, but trust me, this one will cost you nothing and the return on the investment of 10-20 minutes a day is life changing.

Any one of these things can help you sort your money out and make a leap in the right direction. But if you still need a bit of support or a push in the right direction, I have freebies, budget planners, a course and coaching packages available. Good luck and happy leaping!